Navigating the complex landscape of CPF post-death can be daunting. This comprehensive guide delves into the crucial aspects, empowering you with essential knowledge and actionable steps.

1. Understanding CPF Distribution After Death

Upon the demise of a CPF member, the accumulated funds in their three CPF accounts undergo the following distribution process:

- Special Account Savings: 100% transferred to the deceased’s estate or nominee.

- Ordinary Account Savings:

- If 55 or younger: 50% transferred to the estate, 50% to the CPF Retirement Account.

-

If 55 or older:

- If CPF LIFE has not been set up: 50% to the estate, 50% to the MediSave Account.

- If CPF LIFE has been set up: 100% transferred to CPF LIFE.

- MediSave Account Savings:

- If CPF LIFE has been set up: Transferred to CPF LIFE.

- If CPF LIFE has not been set up: 50% to the estate, 50% to the Special Account Savings.

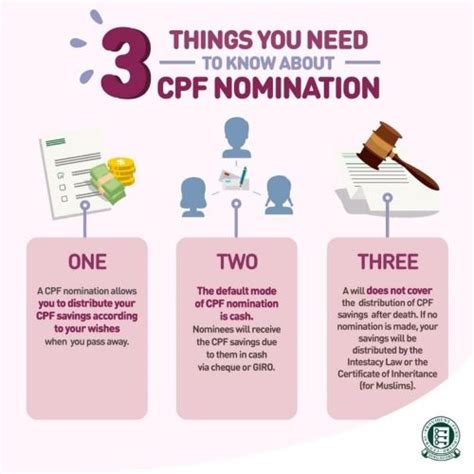

2. CPF Nomination: Ensuring Your Funds Go Where You Want

To ensure that your CPF savings are distributed according to your wishes, consider appointing a CPF nominee. This can be any individual, including your spouse, family member, or close friend. The nominee must be at least 16 years of age and can be updated anytime before your demise.

3. CPF Withdrawal Options for Family Members

Eligible family members can access certain CPF savings of the deceased under the Dependants’ Protection Scheme (DPS). This includes:

- Spouse and unmarried children below 21 or who are full-time students.

- Parents of the deceased who were wholly dependent on them.

The amount of CPF savings available for withdrawal depends on the age of the deceased and the balance in their CPF accounts.

4. Establishing a CPF LIFE Plan: Securing Your Retirement Income

CPF LIFE is a mandatory retirement plan that provides monthly payouts to CPF members upon reaching the age of 65. If the deceased had not set up a CPF LIFE plan, their CPF savings can still be used to purchase an annuity under the CPF LIFE Standard Plan.

5. Estate Planning Considerations

CPF contributions made after the age of 55 are considered part of your estate and subject to estate duty if the total value of your estate exceeds $2 million. Proper estate planning can help minimize estate duty, ensuring that your loved ones receive the maximum possible benefit.

6. Grief and Emotional Support

The loss of a loved one can be a highly emotional experience. Beyond the financial implications, it is crucial to prioritize self-care and seek professional support if needed. Grief counseling and support groups can provide valuable assistance in navigating the challenges of this difficult time.

7. Practical Tips for Beneficiaries

To ensure a smooth process for beneficiaries:

- Notify CPF Board immediately: Inform the CPF Board of the member’s death as soon as possible.

- Gather necessary documents: Collect the deceased’s NRIC, CPF statement, and nomination details.

- Submit claim forms: Lodge the appropriate CPF withdrawal or estate administration forms with the CPF Board.

- Be patient: CPF processing times can vary. Follow up regularly to stay informed of the progress.

Conclusion

Managing CPF post-death involves a combination of legal, financial, and emotional considerations. By understanding the distribution process, appointing a CPF nominee, exploring withdrawal options, and seeking professional support when needed, you can ensure a seamless and respectful transition for your loved ones. Remember, the legacy you leave behind extends beyond financial assets; it is about providing peace of mind and empowering your family to navigate the path ahead with confidence.