Introduction:

In Singapore, the Central Provident Fund (CPF) plays a crucial role in helping individuals purchase their homes. The CPF Ordinary Account (OA) specifically allows members to use their savings to finance their housing loans. As the housing market continues to evolve, it’s essential to understand the maximum CPF amount that can be used for housing loans in 2025.

Maximum Monthly CPF for Housing Loan in 2025

The maximum monthly CPF amount that can be used for housing loans in 2025 is projected to be S$2,500. This amount is subject to change based on future policy decisions and prevailing market conditions.

Eligibility Criteria

To be eligible to use your CPF OA savings for a housing loan, you must meet the following criteria:

- Be a Singapore citizen or Permanent Resident

- Be employed and earning at least S$6,000 per month

- Have sufficient CPF OA savings

- Meet the age and loan tenure requirements

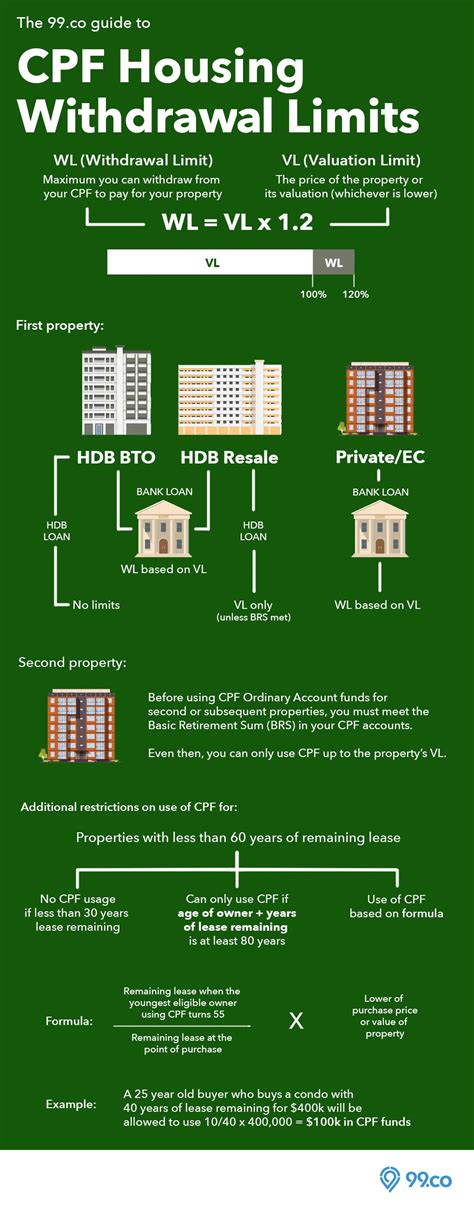

Calculation of CPF Housing Loan Amount

The amount of CPF that can be used for a housing loan is calculated based on the following factors:

- Age of the youngest borrower

- Loan tenure

- Loan amount

- CPF OA balance

- Other CPF deductions and contributions

To determine your exact CPF housing loan eligibility, you can use the CPF Housing Loan Calculator provided by the CPF Board.

Example:

Suppose you are a 30-year-old Singaporean applying for a HDB loan of S$300,000 with a loan tenure of 25 years. Your CPF OA balance is S$100,000. Based on the current CPF withdrawal limits, you can use up to S$2,360 of your CPF OA savings per month towards your housing loan.

Comparison with 2023

The maximum monthly CPF for housing loans in 2025 is expected to remain similar to the current limit of S$2,360. However, it’s important to note that the CPF withdrawal limits are periodically reviewed by the government and may be adjusted in the future.

Implications for Homebuyers

The maximum CPF housing loan amount has a significant impact on the affordability of homes for potential homebuyers. A higher CPF withdrawal limit allows buyers to borrow more from their CPF OA, reducing the need for additional financing from banks. This can translate into lower interest costs and lower monthly mortgage payments.

Considerations for First-Time Homebuyers

For first-time homebuyers, it’s crucial to carefully plan and budget for the purchase of a property. The maximum CPF for housing loans can provide a financial cushion, but it’s important to consider additional expenses such as down payment, stamp duty, legal fees, and renovation costs.

Conclusion

Understanding the maximum CPF for housing loans in 2025 is essential for individuals planning to purchase a property. By using the CPF Housing Loan Calculator and consulting with a financial advisor, you can determine your eligibility for CPF financing and make informed decisions about your home purchase. As the housing market continues to evolve, it’s important to stay informed about changes in CPF policies and regulations to maximize your housing loan options.

Frequently Asked Questions

1. Can I use my CPF savings for an HDB loan and a private housing loan?

Yes, you can use your CPF savings for both HDB and private housing loans. However, the withdrawal limits and eligibility criteria may differ for each type of loan.

2. What happens if I exceed the maximum CPF withdrawal limit?

If you exceed the maximum CPF withdrawal limit, you will be charged a penalty interest of 2.5% per annum on the excess amount withdrawn.

3. How do I apply for a CPF housing loan?

You can apply for a CPF housing loan through your preferred financial institution. The financial institution will assist you with the application process and provide you with the necessary information.