Introduction

In Singapore, the Central Provident Fund (CPF) is a critical savings scheme that helps individuals prepare for retirement, housing, and healthcare expenses. The CPF Retirement Account (RA) is a vital component of this scheme, and topping it up regularly is essential for securing your financial future. This guide will provide you with a comprehensive overview of how to top up your CPF RA, including different methods, eligibility criteria, and key considerations.

Why Top Up Your CPF Retirement Account?

Topping up your CPF RA offers numerous benefits, including:

- Enhanced Retirement Savings: Regular contributions to your RA increase your retirement savings and ensure a more comfortable retirement.

- Tax Benefits: CPF contributions enjoy tax relief of up to S$8,000 per assessment year, reducing your taxable income and saving you money.

- Government Matching Contribution: The government provides a matching contribution of up to S$6,000 per year for eligible individuals. This additional contribution further boosts your retirement savings.

- Investment Opportunities: Your CPF savings can be invested in various growth options through the CPF Investment Scheme, potentially generating higher returns over time.

Eligibility Criteria for CPF RA Top-Ups

To be eligible for CPF RA top-ups, you must:

- Be a Singapore Citizen or Permanent Resident

- Be below the age of 55 for voluntary contributions

- Have sufficient funds in your Ordinary Account (OA) or Special Account (SA) for transfer

Methods of CPF RA Top-Ups

There are several methods available for topping up your CPF RA:

| Method | Description |

|---|---|

| Online (CPF e-Services) | Log in to your CPF account and transfer funds from your OA or SA. |

| ATM | Visit any DBS/POSB, UOB, or OCBC ATM and transfer funds using your NRIC and PIN. |

| Bank Transfer | Submit a funds transfer request from your bank account to your CPF account. |

| GIRO | Set up a monthly GIRO instruction to automatically transfer a fixed amount from your bank account to your CPF RA. |

| Cash at CPF Service Centres | Visit any CPF Service Centre and deposit cash using the Self-Service Kiosks or over the counter. |

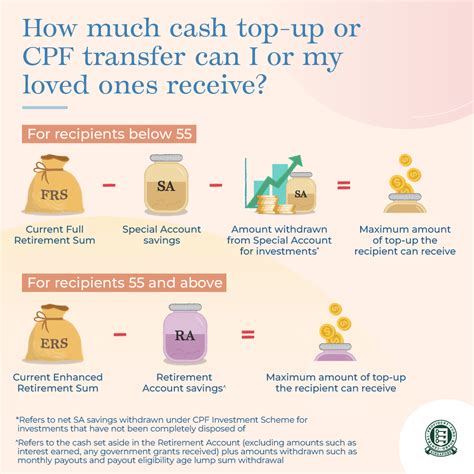

Maximum Top-Up Limits

The maximum amount you can top up to your CPF RA varies depending on your age and CPF contribution history:

| Age Group | CPF Contribution History | Maximum Top-Up Limit |

|---|---|---|

| Below 55 Years Old | No prior CPF contributions | S$7,100 per calendar year |

| Below 55 Years Old | Prior CPF contributions | S$15,100 per calendar year |

| 55 Years Old and Above | N/A | S$7,100 per calendar year |

Factors to Consider Before Topping Up

Before topping up your CPF RA, it’s important to consider the following factors:

- Retirement Goals: Evaluate your anticipated retirement expenses and determine if the additional top-ups will sufficiently supplement your savings.

- Short-Term Financial Needs: Ensure that you have adequate funds to cover immediate expenses and emergencies before committing to CPF top-ups.

- Investment Alternatives: Consider other investment options that may offer higher returns, such as stocks, bonds, or real estate. However, these investments come with their own risks and should be carefully evaluated.

- Tax Implications: The tax benefits of CPF contributions should be weighed against the potential returns from other investments.

Special Considerations for Employers

Employers also play a crucial role in encouraging CPF RA top-ups among their employees:

- Employer Contributions: Employers are required to contribute 17% of an employee’s monthly salary to their CPF accounts. Of this, 7% is automatically allocated to the RA.

- Matching Contributions: The government provides matching contributions of up to S$6,000 per year to employees who make additional top-ups to their RA.

- Employer-Initiated Top-Ups: Employers can also initiate top-ups to their employees’ RA on a voluntary basis.

FAQs

1. Can I withdraw my CPF RA top-ups later?

- No, CPF RA top-ups are locked in until you reach the CPF withdrawal age (currently 55 years old).

2. What happens if I exceed the maximum top-up limit?

- Excess contributions will be refunded to your OA or SA.

3. How can I increase my CPF RA top-up limit?

- You can make prior CPF contributions to your OA or SA to increase your eligibility limit.

4. Are there any tax benefits for employer-initiated top-ups?

- Yes, employer-initiated top-ups are considered employer CPF contributions and qualify for tax relief.

Conclusion

Topping up your CPF Retirement Account is a wise financial decision that can significantly enhance your retirement security. By understanding the different methods, eligibility criteria, and factors to consider, you can make informed decisions and maximize the benefits of CPF contributions. Remember to consult with a financial advisor if you have any specific questions or require further guidance.