SRS Overview

The Supplementary Retirement Scheme (SRS) is a voluntary retirement savings scheme that allows Singaporeans and Permanent Residents to save for their retirement. Contributions to SRS are tax-deductible, and the investment returns are tax-free. This makes SRS a highly attractive way to save for retirement.

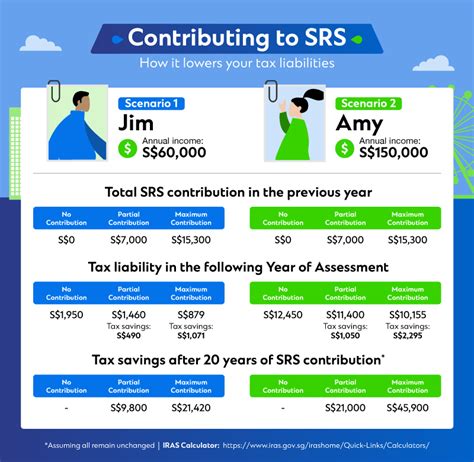

As of 2023, the annual SRS contribution limit is $15,300. This means that you can save up to $15,300 per year in your SRS account and enjoy tax deductions on the contributions.

Benefits of Topping Up SRS

Topping up your SRS account regularly can provide you with a number of benefits:

- Tax savings: Contributions to SRS are tax-deductible, which means that you can reduce your taxable income and save on taxes.

- Investment returns: The investment returns on SRS are tax-free, which means that you can grow your retirement savings faster.

- Retirement security: SRS provides you with a supplementary source of retirement income, which can help you maintain your standard of living in retirement.

How to Top Up SRS Account in 4 Easy Steps

Topping up your SRS account is a simple and straightforward process. You can follow these steps to top up your account:

Step 1: Log in to your SRS account

You can log in to your SRS account online or through your bank’s mobile banking app.

Step 2: Select ‘Top Up Account’

Once you are logged in to your SRS account, select the ‘Top Up Account’ option.

Step 3: Enter the amount you want to top up

Enter the amount that you want to top up into your SRS account.

Step 4: Confirm the top-up

Confirm the top-up amount and click on the ‘Submit’ button.

Your SRS account will be topped up within 2 business days.

Tips and Tricks for Topping Up SRS

Here are a few tips and tricks to help you make the most of your SRS contributions:

- Make regular contributions: It is more beneficial to make regular contributions to SRS over time rather than making a single lump sum contribution. This is because regular contributions will allow you to take advantage of tax deductions and investment returns over a longer period of time.

- Consider an SRS investment plan: Many financial institutions offer SRS investment plans that allow you to invest your SRS funds in a variety of assets, such as stocks, bonds, and mutual funds. Investment plans can provide you with the potential to grow your SRS savings more quickly.

- Take advantage of employer matching contributions: Some employers may offer to match SRS contributions made by their employees. If your employer offers a matching contribution, it is a good idea to take advantage of this benefit.

FAQs About SRS Top-Ups

1. How often can I top up my SRS account?

You can top up your SRS account as often as you like. However, you are only allowed to contribute up to the annual contribution limit of $15,300 per year.

2. Are there any fees for topping up SRS account?

Most banks and financial institutions do not charge fees for topping up SRS account.

3. Can I withdraw my SRS contributions before retirement?

You can withdraw your SRS contributions before retirement if you meet certain conditions. However, you will have to pay a 5% penalty tax on the withdrawn amount.

4. Can I use my SRS account to invest in property?

You can use your SRS account to invest in certain types of property, such as residential properties and commercial properties. However, you will need to meet certain conditions, such as using the property for owner-occupation or renting out the property.

Conclusion

Topping up your SRS account regularly is a great way to save for retirement and enjoy a number of tax benefits. By following the steps outlined above, you can easily top up your SRS account and start growing your retirement savings.

Additional Resources

Tables

Table 1: SRS Annual Contribution Limits

| Year | Contribution Limit |

|---|---|

| 2023 | $15,300 |

| 2022 | $15,300 |

| 2021 | $15,300 |

Table 2: Tax Deductions for SRS Contributions

| Income | Tax Deduction |

|---|---|

| $20,000 | $1,530 |

| $40,000 | $3,060 |

| $60,000 | $4,590 |

Table 3: SRS Investment Options

| Investment Type | Potential Benefits |

|---|---|

| Stocks | High potential returns |

| Bonds | Stable returns |

| Mutual funds | Diversification and professional management |

| Real estate | Potential for capital appreciation and rental income |

Table 4: SRS Withdrawal Rules

| Withdrawal Type | Conditions | Penalty Tax |

|---|---|---|

| Retirement | Age 62 or later | None |

| Disability | Certified disability | None |

| Terminal illness | Certified terminal illness | None |

| Financial hardship | Loss of income, medical expenses | 5% |