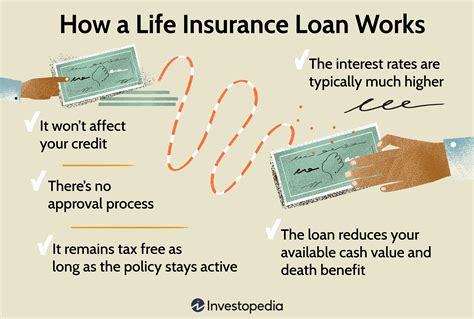

In times of financial emergencies, a life insurance policy can be a valuable asset for individuals and families. One way to access these funds without surrendering the policy is to take a loan against it. This article will provide a comprehensive guide on how to take out a loan from a life insurance policy, covering the eligibility criteria, application process, interest rates, and repayment options, so that you can make informed decisions about leveraging your life insurance for financial assistance.

Understanding Life Insurance Loans

A life insurance loan is a type of secured loan where the policy itself serves as collateral. As compared to traditional loans, life insurance loans typically offer lower interest rates since the policy’s cash value secures the loan.

Eligibility Requirements

To qualify for a life insurance loan, individuals generally need to meet the following criteria:

- Policy Type: Whole life and universal life insurance policies with a cash value component are typically eligible for loans.

- Policy Age: The policy must have been in force for a certain period (e.g., 2-3 years) to accumulate a sufficient cash value.

- Loan-to-Value (LTV) Ratio: Lenders may impose loan limits based on the policy’s cash value. The LTV ratio, which represents the loan amount relative to the cash value, may not exceed 80-90%.

- Health and Financial Status: Some lenders may consider the borrower’s health and financial situation when evaluating eligibility.

Application Process

Obtaining a loan against your life insurance policy typically involves the following steps:

- Contact the Insurance Company: Reach out to the insurance provider that issued your policy to inquire about loan options.

- Submit an Application: Fill out a loan application form and provide supporting documents such as proof of identity and income.

- Policy Review: The insurance company will evaluate your policy and assess your eligibility based on the established criteria.

- Loan Approval: If approved, you will receive details about the loan amount, interest rate, and repayment terms.

- Loan Disbursement: Once the loan agreement is finalized, the approved amount will be disbursed to you.

Key Considerations

Interest Rates

Interest rates for life insurance loans are generally lower than those for personal loans or credit cards but can vary based on factors such as:

- Policy Type: Whole life policies typically have lower interest rates than universal life policies.

- Loan-to-Value Ratio: Higher LTV ratios may lead to slightly higher interest rates.

- Loan Term: Longer loan terms may result in lower monthly payments but higher total interest paid.

Repayment Options

Repayment options for life insurance loans vary depending on the policy and lender, but commonly include:

- Interest-Only Payments: Borrowers may only need to make interest payments during the loan term, with the principal balance due at the end.

- Regular Installments: Monthly payments are fixed and cover both interest and principal, reducing the outstanding balance gradually.

- Flexible Repayment Plans: Some lenders offer flexible repayment schedules that allow borrowers to adjust payments within certain limits.

Repayment Impact on Policy Value:

Repaying the loan plus interest will reduce the policy’s cash value. If the loan is not repaid in full or the policy lapses, the death benefit may be reduced.

Benefits of Life Insurance Loans

- Lower Interest Rates: Compared to other loan options, life insurance loans often offer more favorable interest rates due to the underlying policy collateral.

- No Credit Check: Life insurance loans do not typically require a credit check, potentially making them accessible to individuals with less-than-perfect credit histories.

- Flexibility: The funds from a life insurance loan can be used for a variety of financial needs, such as emergencies, education expenses, or home improvements.

- Minimal Impact on Credit Score: Unlike traditional loans, life insurance loans do not typically impact credit scores, preserving your creditworthiness.

Drawbacks of Life Insurance Loans

- Reduced Death Benefit: As the loan is secured against the policy’s cash value, the death benefit may be reduced until the loan is repaid in full.

- Missed Payments: Failure to repay the loan as agreed can result in penalties or even policy lapse, potentially jeopardizing the policy’s benefits.

- Loan Limits: The amount you can borrow against your life insurance policy may be limited by the policy’s cash value and loan-to-value ratio restrictions.

- Additional Fees: Some insurance companies may charge administrative or maintenance fees associated with life insurance loans.

Table 1: Key Features of Life Insurance Loans

| Feature | Description |

|---|---|

| Eligibility | Whole life and universal life policies with cash value |

| Interest Rates | Lower than personal loans or credit cards |

| Loan Amounts | Limited by policy’s cash value and loan-to-value ratio |

| Repayment Options | Interest-only payments, regular installments, flexible plans |

| Impact on Policy | Death benefit may be reduced until loan is repaid |

Table 2: Benefits and Drawbacks of Life Insurance Loans

| Benefits | Drawbacks |

|---|---|

| Lower interest rates | Reduced death benefit |

| No credit check | Potential for missed payments |

| Flexibility | Loan limits |

| Minimal impact on credit score | Additional fees |

Expert Insights

“Life insurance loans can be a valuable financial tool for policyholders in times of need,” says Jason Kramer, a financial advisor with over 20 years of experience. “However, it’s crucial to understand the potential implications on your policy’s death benefit and to approach loan options with caution.”

Alternative Funding Options

If a life insurance loan is not suitable, consider these alternative funding options:

- Personal loans: Unsecured loans with higher interest rates but may be more accessible for individuals with good credit.

- Home equity loans or lines of credit: Secured loans using your home equity as collateral, but can come with risks if property values decline.

- Credit cards: Can be convenient for small expenses, but carry high interest rates and can damage credit if not managed responsibly.

Table 3: Alternative Funding Options

| Option | Features |

|---|---|

| Personal loans | Higher interest rates, unsecured |

| Home equity loans/lines of credit | Secured by home equity, potential risks |

| Credit cards | Convenient for small expenses, high interest rates |

Table 4: Tips for Evaluating Funding Options

| Factor | Considerations |

|---|---|

| Interest rates | Compare rates from multiple lenders |

| Loan terms | Choose a term that fits your financial situation |

| Loan limits | Determine if the loan amount meets your needs |

| Repayment options | Consider the flexibility and impact on your budget |

| Impact on credit | Understand how the loan may affect your credit score |

Conclusion

Taking a loan against a life insurance policy can be a viable option for individuals seeking financial assistance, provided they meet the eligibility criteria and understand the potential implications on the death benefit. By carefully considering the pros and cons, researching alternative funding options, and consulting with financial advisors, individuals can make informed decisions about leveraging their life insurance policies for financial support while preserving the policy’s long-term benefits.