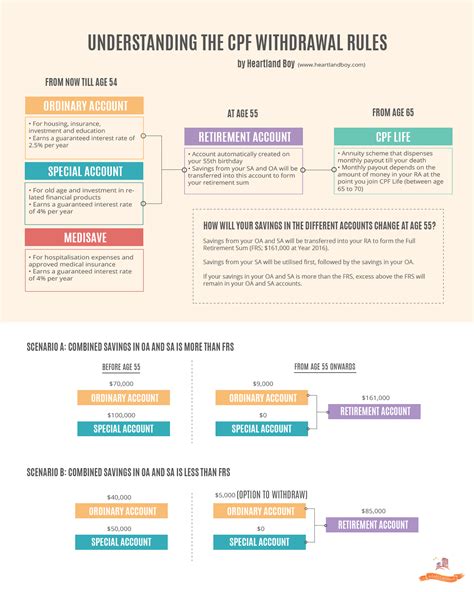

Understanding Your CPF Withdrawal Options

At age 55, CPF members in Singapore have the option to withdraw a significant portion of their CPF savings to supplement their retirement income or meet other financial needs. The amount of money you can withdraw will depend on several factors, including your age, marital status, and the amount of savings you have accumulated in your CPF accounts.

CPF Withdrawal Rules at Age 55

Under the CPF LIFE scheme, CPF members who reach age 55 can withdraw up to $100,000 from their Ordinary Account (OA) and Special Account (SA) combined. This is known as the “Basic Retirement Sum” (BRS).

For members who are married and have reached age 55

- Males: Can withdraw up to 90% of their OA and SA balances, up to a maximum of $200,000.

- Females: Can withdraw up to 85% of their OA and SA balances, up to a maximum of $185,000.

For single members who have reached age 55

- Can withdraw up to 95% of their OA and SA balances, up to a maximum of $190,000.

Pain Points and Motivations

Pain Points

- Uncertainty about the amount of CPF they can withdraw at age 55.

- Concerns about having sufficient retirement savings after withdrawing CPF funds.

- Difficulty understanding the complex CPF withdrawal rules.

Motivations

- Need to supplement retirement income.

- Want to use CPF funds to pay for housing or other major expenses.

- Desire to have more financial flexibility in retirement.

Common Mistakes to Avoid

- Withdrawing too much CPF: This can reduce your retirement savings and increase your risk of running out of money in old age.

- Not considering the impact of taxes: CPF withdrawals are subject to income tax, so you may end up paying more taxes than you anticipate.

- Not using CPF funds wisely: It’s important to use CPF withdrawals wisely to ensure they provide long-term financial benefits.

Creative New Word for Generating Ideas: “CPFication”

The term “CPFication” can be used to describe the process of using CPF funds to achieve financial goals, such as purchasing a home or securing retirement income. This concept encourages CPF members to think creatively about how they can leverage their CPF savings to enhance their financial well-being.

Tables for Understanding Withdrawal Options

Table 1: Basic Retirement Sum (BRS) Withdrawal Limits

| Age | Married (Married Couples) | Single |

|---|---|---|

| 55 | $100,000 | $100,000 |

Table 2: Maximum Withdrawal Limits for Members Married on or After 01 January 2003

| Age | Males | Females |

|---|---|---|

| 55 | 90% of OA + SA balances (up to $200,000) | 85% of OA + SA balances (up to $185,000) |

Table 3: Maximum Withdrawal Limits for Single Members

| Age | Maximum Withdrawal Limit |

|---|---|

| 55 | 95% of OA + SA balances (up to $190,000) |

Table 4: CPF Withdrawal Tax Rates

| Withdrawal Amount | Tax Rate |

|---|---|

| Up to $20,000 | 0% |

| $20,001 to $30,000 | 5% |

| $30,001 to $40,000 | 10% |

| $40,001 to $80,000 | 15% |

| Over $80,000 | 20% |

Conclusion

Withdrawing CPF funds at age 55 is a major decision that can significantly impact your financial future. By understanding the withdrawal rules, considering your individual circumstances, and avoiding common mistakes, you can make informed decisions about how to use your CPF savings to achieve your retirement goals. Remember to consult with financial advisors if you have questions or need personalized guidance.