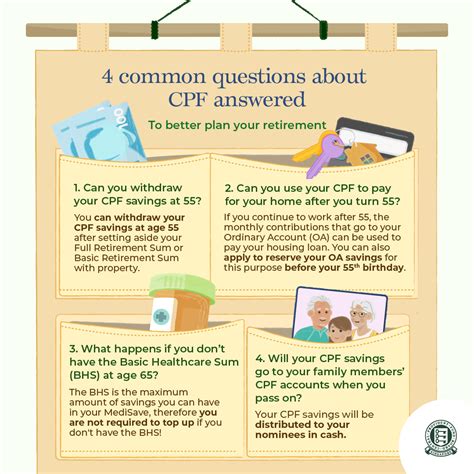

The Central Provident Fund (CPF) is a compulsory savings scheme in Singapore that helps Singaporeans save for their retirement, healthcare, and housing needs. Members can start withdrawing their CPF savings from the age of 55.

Minimum Sum Scheme

The Minimum Sum Scheme (MSS) is a CPF scheme that determines the minimum amount of CPF savings that members must set aside for their retirement. The MSS amount varies depending on the member’s age and is reviewed every five years. For members who reach age 55 in 2023, the MSS amount is S$93,000.

CPF Withdrawal Options

Once members reach the age of 55, they can withdraw their CPF savings in the following ways:

- CPF LIFE: CPF LIFE is an annuity scheme that provides members with a monthly payout for life. Members can choose from different CPF LIFE plans, each with its own payout terms and conditions.

- CPF Investment Scheme (CPFIS): CPFIS is a government-managed investment scheme that allows members to invest their CPF savings in a range of investment products, such as unit trusts and bonds.

- CPF Ordinary Account (OA): Members can withdraw their OA savings in a lump sum or in installments. OA savings can be used for a variety of purposes, such as purchasing a property, paying for education, or investing.

- CPF Special Account (SA): Members can withdraw their SA savings in a lump sum or in installments. SA savings can be used for a variety of purposes, such as purchasing a property, paying for education, or investing.

Factors to Consider When Withdrawing CPF Savings

When considering withdrawing CPF savings, members should take into account the following factors:

- Retirement needs: Members should ensure that they have sufficient CPF savings to meet their retirement needs, such as healthcare costs and living expenses.

- Investment goals: Members who wish to invest their CPF savings should consider their investment goals and risk tolerance.

- Tax implications: Withdrawals from CPF accounts may be subject to income tax.

Strategies for Withdrawing CPF Savings

There are a number of strategies that members can use to withdraw their CPF savings in a way that meets their needs. These strategies include:

- Withdrawing OA savings first: OA savings are taxed at a lower rate than SA savings. Members can withdraw their OA savings in a lump sum or in installments.

- Deferring SA withdrawals: Deferring SA withdrawals can allow members to accumulate more interest on their savings. Members can defer SA withdrawals until they reach the age of 65.

- Investing CPF savings: Members can invest their CPF savings in a range of investment products, such as unit trusts and bonds. Investing CPF savings can help members to grow their savings over time.

Conclusion

Withdrawing CPF savings is an important decision that can have a significant impact on members’ retirement. Members should carefully consider their needs and goals before making any decisions about withdrawing their CPF savings.

Tables

Table 1: CPF Withdrawal Options

| Option | Description |

|---|---|

| CPF LIFE | Annuity scheme that provides members with a monthly payout for life |

| CPF Investment Scheme (CPFIS) | Government-managed investment scheme that allows members to invest their CPF savings in a range of investment products |

| CPF Ordinary Account (OA) | Members can withdraw their OA savings in a lump sum or in installments |

| CPF Special Account (SA) | Members can withdraw their SA savings in a lump sum or in installments |

Table 2: Minimum Sum Scheme (MSS) Amounts

| Age at 55 | Minimum Sum Amount (S$) |

|---|---|

| 55 (2023) | 93,000 |

| 55 (2024) | 95,500 |

| 55 (2025) | 98,100 |

Table 3: CPF Withdrawal Tax Rates

| Account Type | Lump Sum Withdrawal | Gradual Withdrawal |

|---|---|---|

| CPF Ordinary Account (OA) | 0% | 0% |

| CPF Special Account (SA) | 5% | 0% |

Table 4: Strategies for Withdrawing CPF Savings

| Strategy | Description |

|---|---|

| Withdraw OA savings first | OA savings are taxed at a lower rate than SA savings. Members can withdraw their OA savings in a lump sum or in installments. |

| Defer SA withdrawals | Deferring SA withdrawals can allow members to accumulate more interest on their savings. Members can defer SA withdrawals until they reach the age of 65. |

| Invest CPF savings | Members can invest their CPF savings in a range of investment products, such as unit trusts and bonds. Investing CPF savings can help members to grow their savings over time. |