Introduction

In the competitive real estate market, buyers often consider various strategies to reduce their tax liability. One such strategy is the use of living trusts, which can provide asset protection and estate planning benefits. However, it’s crucial to understand the implications of living trusts on additional buyer stamp duty (ABSD) in certain jurisdictions. This article delves into the interplay between living trusts and ABSD, exploring the potential impact on property purchases.

What is ABSD?

ABSD is a form of property tax imposed on the purchase of residential properties in certain countries. It is levied in addition to the regular stamp duty and is designed to curb speculative buying and maintain market stability. The exact rates and conditions of ABSD vary from jurisdiction to jurisdiction.

Living Trusts and ABSD

A living trust is a legal arrangement where an individual transfers ownership of assets to a trustee, who manages and distributes the assets according to the grantor’s instructions. Living trusts offer several advantages, such as asset protection, probate avoidance, and tax efficiency.

In some jurisdictions, living trusts can also be used to reduce ABSD. By transferring ownership of the property to a living trust before purchasing, the buyer may be able to avoid paying ABSD that would otherwise be levied on the purchase price.

Implications for Buyers

Advantages:

- Potential ABSD savings: If the living trust structure is properly implemented, buyers can potentially reduce or eliminate ABSD liability.

- Estate planning benefits: Living trusts provide a comprehensive estate plan, ensuring that the property is managed and distributed according to the grantor’s wishes.

- Asset protection: Trusts can safeguard the property from creditors and other legal claims.

Disadvantages:

- Complexity: Setting up a living trust can be complex and requires legal expertise.

- Cost: Legal fees and other expenses associated with the trust setup can be substantial.

- Tax implications: Income generated by the property held in trust may be subject to different tax rules.

Considerations for Buyers

When considering the use of a living trust to reduce ABSD, buyers should carefully evaluate the following factors:

- Jurisdiction: The laws and regulations regarding living trusts, ABSD, and property ownership vary across jurisdictions.

- Property value: The higher the property value, the greater the potential ABSD savings.

- Tax implications: Buyers should consider the potential tax consequences of holding the property in a trust.

- Legal implications: Establishing a living trust is a legal matter, and buyers should seek professional legal advice to ensure compliance and avoid any legal pitfalls.

Tips for Buyers

- Consult an attorney: Engage a qualified attorney to guide you through the process and ensure that the living trust is properly implemented.

- Explore other options: Consider other strategies to reduce ABSD, such as purchasing properties together with family members or utilizing government grants and incentives.

- Weigh the pros and cons: Carefully consider the advantages and disadvantages of using a living trust to avoid ABSD before making a decision.

Case Study

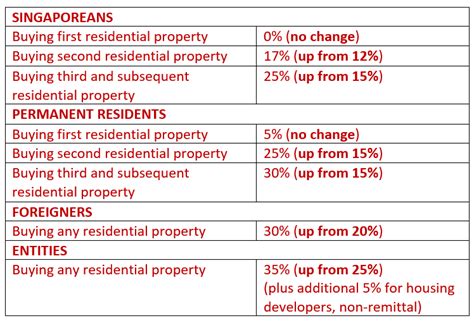

In Singapore, ABSD rates for residential properties purchased by individuals range from 12% to 24%, depending on the residency status and purchase history of the buyer. A buyer who purchases a $1 million property as an individual would be liable for $120,000 in ABSD.

By transferring the property to a living trust before purchasing, the individual could potentially avoid paying ABSD, resulting in significant savings.

Table 1: ABSD Rates in Selected Jurisdictions

| Jurisdiction | ABSD Rate |

|---|---|

| Singapore | 12%-24% |

| Hong Kong | 15%-30% |

| Australia | 0%-7% |

| United Kingdom | 3%-12% |

Table 2: Advantages and Disadvantages of Living Trusts for ABSD

| Advantages | Disadvantages |

|---|---|

| Potential ABSD savings | Complexity in setup and management |

| Estate planning benefits | Legal and tax implications |

| Asset protection | Additional costs and expenses |

Table 3: Considerations for Buyers Using Living Trusts for ABSD

| Factor | Considerations |

|---|---|

| Jurisdiction | Legal and regulatory framework for living trusts and ABSD |

| Property value | Impact on potential ABSD savings |

| Tax implications | Income and capital gains tax treatment of trust-held properties |

| Legal implications | Compliance with legal requirements and avoidance of pitfalls |

Table 4: Tips for Buyers Using Living Trusts for ABSD

| Tip | Explanation |

|---|---|

| Consult an attorney | Seek professional guidance to ensure proper implementation |

| Explore other options | Consider alternative strategies to reduce ABSD |

| Weigh the pros and cons | Evaluate the advantages and disadvantages carefully |

Conclusion

Using a living trust to reduce ABSD can be a viable strategy, but it requires careful consideration and planning. Buyers should consult legal and financial professionals to thoroughly assess the implications and determine if a living trust is the right solution for their specific circumstances. By understanding the complexities of ABSD and living trusts, buyers can make informed decisions and optimize their property purchases.