1. Introduction

Singapore, known for its vibrant economy and low tax rates, has a progressive income tax system that requires residents and non-residents to pay taxes on their income earned in the country. Understanding the eligibility criteria and tax obligations is crucial for individuals and businesses operating in Singapore. This guide provides a comprehensive overview of who needs to pay income tax in Singapore by 2025.

2. Residency Status and Tax Liability

Residency status is a key factor in determining tax liability in Singapore. Individuals are classified as either residents or non-residents based on their physical presence in the country.

2.1 Residents

Residents are individuals who have established a permanent home in Singapore or have been physically present in the country for 183 days or more in a calendar year. Residents are subject to income tax on their worldwide income.

2.2 Non-Residents

Non-residents are individuals who do not meet the residency criteria. They are subject to income tax only on their income earned in Singapore.

3. Taxable Income

Taxable income in Singapore refers to the net income after deducting allowable expenses and tax reliefs from gross income. Gross income includes all income earned in Singapore, regardless of its source. Allowable expenses are specific deductions that reduce taxable income, such as business expenses, certain personal expenses, and charitable donations.

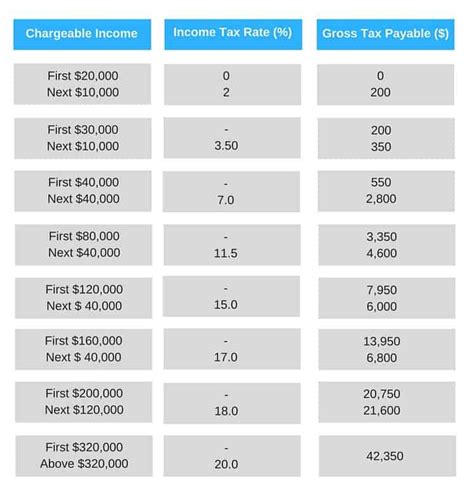

4. Tax Rates

Singapore’s income tax rates are progressive, meaning that higher income earners pay a higher percentage of tax. The income tax rates for individuals and businesses for 2025 are as follows:

4.1 Individuals

| Taxable Income Range (SGD) | Tax Rate (%) |

|---|---|

| 0 – 20,000 | 0 |

| 20,001 – 40,000 | 2 |

| 40,001 – 80,000 | 5 |

| 80,001 – 120,000 | 7 |

| 120,001 – 400,000 | 11 |

| 400,001 and above | 13 |

4.2 Businesses

| Company Type | Tax Rate (%) |

|---|---|

| Private Limited Companies | 17 |

| Public-Listed Companies | 22 |

5. Tax Exemptions and Reliefs

Singapore offers various tax exemptions and reliefs to reduce the tax burden on individuals and businesses. These include:

- Personal Income Tax Relief (PITR): This is a tax credit of up to SGD 5,000 for individuals.

- Earned Income Relief (EIR): This is a tax credit of up to SGD 1,000 for individuals who earn employment income.

- CPF Contributions: Contributions to the Central Provident Fund (CPF) are tax-deductible up to certain limits.

- Corporate Income Tax Exemption: New start-up companies can enjoy a 75% tax exemption on the first SGD 100,000 of taxable income for the first three consecutive years of assessment.

6. Tax Filing Process

Individuals and businesses are required to file their income tax returns annually with the Inland Revenue Authority of Singapore (IRAS). The tax filing season typically runs from March to April each year.

7. Conclusion

Understanding who needs to pay income tax in Singapore is essential for ensuring compliance with tax laws. Residents and non-residents, individuals and businesses, are subject to different tax obligations based on their residency status, income, and tax reliefs available. By staying informed about the latest tax regulations and seeking professional advice if needed, taxpayers can ensure accurate tax filing and avoid penalties.