Seeking the Best Returns on Fixed Deposits

Are you looking for the most lucrative fixed deposit (FD) interest rates in Singapore? Whether you’re an individual seeking secure returns or an institution managing large sums, it’s essential to stay updated on the latest market offerings. Our comprehensive guide will unveil the top 5 FD interest rates available in Singapore for 2025, empowering you to maximize your earnings.

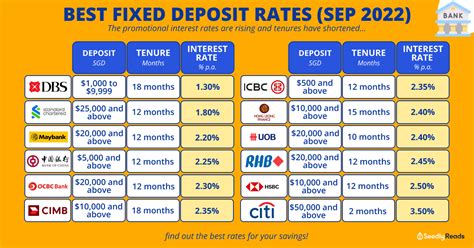

1. DBS Multiplier Account: 3.88% p.a.

DBS’s Multiplier Account stands out with its impressive 3.88% p.a. interest rate, one of the highest in the market. This account combines the benefits of a savings and FD account, offering high returns while maintaining easy access to your funds.

2. OCBC 360 Account: 3.65% p.a.

OCBC’s 360 Account offers a competitive 3.65% p.a. interest rate, making it an excellent option for those looking for a balanced mix of returns and flexibility. This account rewards customers for fulfilling certain criteria, such as maintaining a minimum account balance and making regular transactions.

3. UOB One Account: 3.58% p.a.

UOB One Account offers a competitive 3.58% p.a. interest rate with no lock-in period. This account is ideal for those who prioritize liquidity and the freedom to access their funds whenever needed.

4. Citibank Singapore SmartWealth FD: 3.50% p.a.

Citibank’s Singapore SmartWealth FD offers a steady 3.50% p.a. interest rate for a lock-in period of 18 months. This account is suitable for those willing to commit their funds for a slightly longer duration to earn higher returns.

5. Standard Chartered Bonus$aver: 3.45% p.a.

Standard Chartered’s Bonus$aver offers a solid 3.45% p.a. interest rate for a lock-in period of 12 months. This account is a good option for those seeking a competitive return with a moderate lock-in period.

Factors to Consider When Choosing an FD Interest Rate

- Tenor: Interest rates vary depending on the duration of the FD. Longer tenors typically offer higher rates.

- Lock-in Period: FDs with shorter lock-in periods allow you to access your funds sooner, but may offer lower rates.

- Minimum Deposit: Some FDs require a minimum deposit to qualify for the highest interest rates.

- Additional Features: Some FDs offer additional features such as flexibility to withdraw funds, free withdrawal charges, and insurance coverage.

Effective Strategies for Optimizing FD Returns

- Maximize Tenor: Choose the longest tenor possible to lock in higher interest rates.

- Consider Lock-in Periods: If you can commit your funds for longer, opt for FDs with lock-in periods to earn higher returns.

- Negotiate with Banks: Don’t hesitate to negotiate with banks for better interest rates, especially if you have a large deposit.

- Take Advantage of Promotions: Banks often offer special promotions and bonuses for new FD customers.

Common Mistakes to Avoid

- Not Comparing Rates: Always compare the interest rates offered by different banks before opening an FD account.

- Withdrawing Funds Prematurely: Breaking a FD before the end of its tenor typically results in penalties and reduced interest earnings.

- Choosing the Wrong Tenor: Selecting a tenor that is too short can lead to lower returns, while choosing a tenor that is too long can prevent you from accessing your funds when needed.

Pros and Cons of FD Accounts

Pros:

- Guaranteed Returns: FD interest rates are fixed, providing a guaranteed return on your investment.

- Secure Investment: FDs are considered one of the safest investment options, backed by the Monetary Authority of Singapore’s depositor protection scheme.

- Low Risk: FDs protect your principal investment from market fluctuations.

Cons:

- Limited Liquidity: FD accounts typically have lock-in periods, restricting your ability to access your funds during that time.

- Inflation Risk: FD interest rates may not outpace inflation, resulting in a diminished purchasing power over time.

- Opportunity Cost: FD returns may be lower than those offered by other investment options, such as stocks or bonds.

Introducing a New Word: FDepreciation

To further enhance your understanding of FDs, let’s introduce a creative new word: FDepreciation. This term refers to the decrease in the value of an FD investment due to inflation over time. By incorporating this concept into your financial planning, you can make more informed decisions and protect your returns from the impact of rising prices.

Generate Ideas for New FD Applications

- FD Investment Linked to Index: Create FDs that track a particular market index, such as the Straits Times Index or FTSE 100, offering returns linked to the performance of the underlying index.

- FDs with Customizable Maturities: Introduce FDs that allow customers to choose their own maturities, offering flexibility and cater to their individual investment goals.

- FDs with Performance Bonuses: Offer FDs that reward customers for achieving certain financial milestones, such as maintaining a certain account balance or making a specific number of transactions.

Useful Tables

Table 1: Top 5 FD Interest Rates in Singapore for 2025

| Bank | Interest Rate | Tenor | Lock-in Period |

|---|---|---|---|

| DBS Multiplier Account | 3.88% p.a. | N/A | N/A |

| OCBC 360 Account | 3.65% p.a. | N/A | N/A |

| UOB One Account | 3.58% p.a. | N/A | No |

| Citibank Singapore SmartWealth FD | 3.50% p.a. | 18 months | Yes |

| Standard Chartered Bonus$aver | 3.45% p.a. | 12 months | Yes |

Table 2: Factors to Consider When Choosing an FD Interest Rate

| Factor | Description |

|---|---|

| Tenor | Duration of the FD |

| Lock-in Period | Period during which funds cannot be withdrawn |

| Minimum Deposit | Minimum amount required to open an FD |

| Additional Features | Benefits or perks offered with the FD, such as flexibility or insurance coverage |

Table 3: Effective Strategies for Optimizing FD Returns

| Strategy | Description |

|---|---|

| Maximize Tenor | Choose the longest tenor possible to lock in higher interest rates |

| Consider Lock-in Periods | Opt for FDs with lock-in periods if you can commit your funds for longer |

| Negotiate with Banks | Discuss with banks to negotiate better interest rates, especially for larger deposits |

| Take Advantage of Promotions | Look out for special promotions and bonuses offered by banks |

Table 4: Common Mistakes to Avoid

| Mistake | Description |

|---|---|

| Not Comparing Rates | Failing to compare FD interest rates offered by different banks |

| Withdrawing Funds Prematurely | Breaking a FD before its end often results in penalties and reduced earnings |

| Choosing the Wrong Tenor | Selecting a tenor that is too short can lead to lower returns, while choosing a tenor that is too long can restrict access to funds |