Introduction

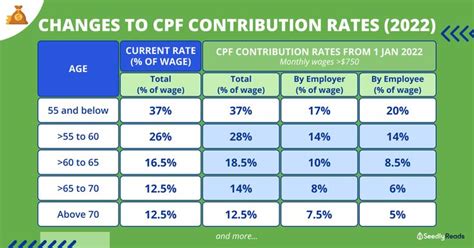

In 2023, the retirement age in Singapore was raised from 62 to 65, with further plans to gradually increase it to 68 by 2028. Consequently, the Central Provident Fund (CPF) contribution rates for Permanent Residents (PRs) will also undergo adjustments over the next few years. This article aims to provide a comprehensive overview of PR 2nd Year CPF Contribution Rates in 2025.

Current PR CPF Contribution Rates

Currently, PRs are subject to lower CPF contribution rates compared to Singapore Citizens (SCs). However, these rates are set to increase gradually over the coming years. In their second year of employment, PRs contribute at the following rates:

| Category | Employee Contribution | Employer Contribution |

|---|---|---|

| Ordinary Account (OA) | 23.5% | 17% |

| Special Account (SA) | 5% | 5% |

2025 PR CPF Contribution Rate Changes

In 2025, the PR 2nd Year CPF Contribution Rate for OA will increase from 23.5% to 24%. Likewise, the employer contribution rate for OA will also increase from 17% to 18%.

| Category | Employee Contribution | Employer Contribution |

|---|---|---|

| Ordinary Account (OA) | 24% | 18% |

| Special Account (SA) | 5% | 5% |

Comparison with SC CPF Contribution Rates

While the PR 2nd Year CPF Contribution Rates are lower than those of SCs, they are still significantly higher than the rates in other countries. For instance, the average CPF contribution rate in Malaysia is only 11%, while in Thailand it is 5%.

| Country | Employee Contribution | Employer Contribution |

|---|---|---|

| Singapore (PR) | 24% | 18% |

| Singapore (SC) | 20% | 17% |

| Malaysia | 11% | 13% |

| Thailand | 5% | 5% |

Impact on PR Retirement Savings

The increase in PR CPF contribution rates will have a significant impact on their retirement savings. According to the CPF Board, a PR earning a monthly salary of S$3,000 will contribute an additional S$180 per month to their CPF account in 2025. Over a 30-year career, this amounts to an additional S$64,800 in retirement savings.

Conclusion

The increase in PR 2nd Year CPF Contribution Rates in 2025 is a necessary step to ensure that PRs have adequate retirement savings. However, the government should also consider providing additional support to PRs who may face difficulties in meeting the higher contribution rates. By working together, we can ensure that all PRs have a secure financial future in Singapore.