Greetings, property enthusiasts and aspiring homeowners! Singapore’s property market is constantly evolving, with new regulations and policies coming into play to ensure stability and affordability. To help you navigate these changes and make informed decisions, we’ve compiled a comprehensive guide to the latest rules for buying property in Singapore.

The Mortgage Servicing Ratio (MSR)

Introduced in 2022, the MSR limits the amount of debt you can take on when applying for a home loan. It affects both your Total Debt Servicing Ratio (TDSR) and your Mortgage Servicing Ratio (MSR).

- TDSR: This calculation limits your total debt payments, including home loans, car loans, and credit card bills, to 55% of your monthly income.

- MSR: The MSR specifically limits your mortgage payments to 60% of your monthly income.

By implementing these measures, the government aims to reduce financial risks and ensure that homeowners can comfortably afford their monthly mortgage payments.

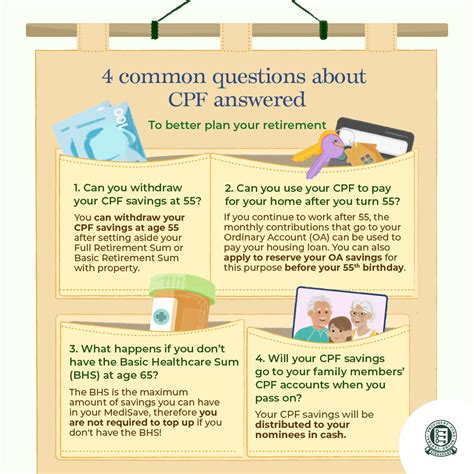

Enhanced Central Provident Fund (CPF) Usage

For first-time homebuyers, the government has enhanced the usage of CPF funds.

- Higher CPF Loan Limits: You can now borrow up to 90% of the property’s purchase price or valuation, whichever is lower, using your CPF savings. This provides a significant boost to your down payment.

- Enhanced CPF Housing Grant: The CPF Housing Grant, which provides financial assistance to eligible first-time buyers, has been increased. For HDB flats, the grant can be up to $80,000, while for private properties, it can be up to $50,000.

These enhancements aim to make homeownership more accessible for first-time buyers.

New Property Cooling Measures

To curb speculation and keep property prices within reach of the majority, the government has introduced cooling measures.

- Additional Buyer’s Stamp Duty (ABSD): This tax is levied on foreigners, Singapore Permanent Residents (PRs), and Singaporean citizens who own multiple properties. The ABSD rates vary depending on the number of properties owned.

- Seller’s Stamp Duty (SSD): This tax is imposed on sellers who dispose of their private residential property within a certain timeframe after acquiring it. The SSD rates gradually decrease over three to four years, incentivizing owners to hold their properties for a longer period.

These measures aim to discourage excessive property ownership and speculation.

New HDB Policies

The Housing & Development Board (HDB) has also implemented new policies to ensure fairness and affordability.

- Reduced Grant Quantum for BTO Flats: To prioritize first-time homebuyers, the grant quantum for Build-To-Order (BTO) flats has been reduced.

- Enhanced Income Ceiling for HDB Flats: The income ceiling for HDB flat eligibility has been raised to $14,000 per month for families and $7,000 per month for singles.

- New Flat Launch System: HDB has introduced a new flat launch system that aims to provide buyers with more time to plan and make informed decisions.

These policies aim to make HDB flats more affordable and accessible to eligible buyers.

Table: Mortgage Servicing Ratios and CPF Loan Limits

| Loan Type | Maximum TDSR | Maximum MSR | Maximum CPF Loan Limit |

|---|---|---|---|

| HDB Loan | 55% | 60% | 90% |

| Bank Loan | 55% | 60% | 80% |

Table: Additional Buyer’s Stamp Duty (ABSD) Rates

| Number of Properties Owned | Citizen/PR Rate | Foreigner Rate |

|---|---|---|

| 1st | 12% | 20% |

| 2nd | 17% | 25% |

| 3rd and subsequent | 25% | 30% |

Table: Seller’s Stamp Duty (SSD) Rates

| Holding Period | Citizen/PR Rate | Foreigner Rate |

|---|---|---|

| Within 1 year | 16% | 20% |

| Between 1 and 2 years | 12% | 15% |

| Between 2 and 3 years | 8% | 10% |

| Between 3 and 4 years | 4% | 5% |

| After 4 years | 0% | 0% |

Table: HDB Flat Eligibility and Income Ceiling

| Type of Flat | Income Ceiling |

|---|---|

| 2-Room Flexi | $14,000 |

| 3-Room and 4-Room | $14,000 |

| 5-Room and Executive | $14,000 |

| Studio Apartment | $7,000 |

Strategies for Navigating the New Rules

- Explore Government Schemes: Take advantage of various government schemes and grants to reduce your financial burden.

- Shop Around for Mortgages: Compare interest rates and loan terms from different banks to secure the best deal.

- Consider HDB Flats: HDB flats offer affordability and stability, especially for first-time homebuyers.

- Plan for Long-Term Occupancy: Cooling measures incentivize owning properties for a longer period.

- Seek Professional Advice: Consult with a property agent or financial planner for personalized guidance.

Pros and Cons of the New Rules

Pros:

- Stabilize Property Prices: Cooling measures aim to prevent excessive price increases and speculation.

- Protect Homebuyers: The MSR ensures that homebuyers can afford their monthly mortgage payments.

- Promote Fair Competition: Enhanced CPF usage and HDB policies prioritize first-time buyers.

Cons:

- Reduced Flexibility for Investors: Cooling measures discourage multiple property ownership.

- Higher Costs for Foreigners: ABSD rates can make property ownership expensive for foreigners.

- Longer Waiting Times: The new HDB flat launch system may delay homeownership timelines.

FAQs

-

When was the MSR implemented?

Answer: June 29, 2022 -

What is the maximum CPF loan limit for HDB flats?

Answer: 90% of the purchase price or valuation -

What is the ABSD rate for first-time homebuyers who are citizens or PRs?

Answer: 12% -

What is the income ceiling for HDB flat eligibility for families?

Answer: $14,000 per month -

How long must I hold my private property before selling it to avoid SSD?

Answer: 4 years -

What is the purpose of the HDB flat launch system?

Answer: To provide buyers with more time to plan and make informed decisions -

Can I borrow more than 80% of the property price using a bank loan?

Answer: No, the maximum CPF loan limit for bank loans is 80%. -

Is it still possible to buy multiple properties in Singapore?

Answer: Yes, but it is subject to additional costs, such as ABSD and SSD.