Introduction

The Central Provident Fund (CPF) is a comprehensive savings scheme designed to help Singaporeans accumulate funds for their retirement, healthcare, and housing needs. As you approach the age of 55, you become eligible to withdraw a portion of your CPF savings, providing you with a financial cushion and flexibility during your golden years. This article provides a comprehensive guide on how much CPF you can withdraw before 2025, exploring the different withdrawal options, eligibility criteria, and factors that influence your withdrawal amount.

Withdrawal Options and Eligibility

At the age of 55, CPF members have two main withdrawal options:

-

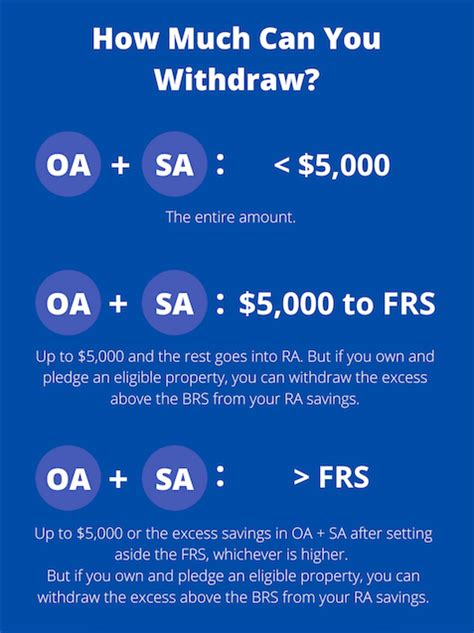

Basic Retirement Sum (BRS) Withdrawal: This is the minimum amount you can withdraw from your CPF Ordinary Account (OA) and Special Account (SA). The BRS is adjusted periodically to ensure that it keeps pace with inflation and rising living costs. For those reaching 55 in 2023, the BRS is set at $93,000.

-

Full Retirement Sum (FRS) Withdrawal: This is the maximum amount you can withdraw from your OA and SA. The FRS is also adjusted periodically and is currently set at $186,000 for those reaching 55 in 2023.

Eligibility for Withdrawal:

To be eligible for CPF withdrawal, you must meet the following criteria:

- Be a Singapore Citizen or Permanent Resident

- Have reached the age of 55

- Have met the minimum CPF contribution requirements

Factors Influencing Withdrawal Amount

The amount of CPF you can withdraw depends on several factors:

- Age: The younger you are when you withdraw, the less you can withdraw. This is because your CPF savings have had less time to accumulate interest.

- CPF Contributions: The more CPF contributions you have made throughout your working life, the higher your CPF balance and, therefore, the more you can withdraw.

- Investment Returns: The returns your CPF investments have generated over the years will also impact your withdrawal amount.

Step-by-Step Guide to Withdraw CPF

Withdrawing CPF is a straightforward process that can be done online or through CPF Service Centres. Here’s a step-by-step guide:

-

Check Your Eligibility: Log in to your CPF online account to determine if you meet the eligibility criteria.

-

Choose a Withdrawal Option: Decide whether you want to withdraw the BRS or FRS amount.

-

Submit Your Application: Fill out the online withdrawal form or visit a CPF Service Centre to submit your application.

-

Receive Payment: Once your application is processed, your CPF withdrawal amount will be credited to your bank account within a few days.

Additional Withdrawal Options

In addition to the BRS and FRS withdrawals, there are several other withdrawal options available:

- Enhanced Retirement Sum (ERS) Scheme: This scheme allows you to top up your CPF savings to reach the FRS amount. Members who join the ERS are eligible for an additional government top-up.

- Retirement Account (RA): A portion of your CPF savings is set aside in your RA at age 55. You can withdraw this amount gradually from age 65 onwards.

- CPF LIFE: CPF LIFE is an annuity scheme that provides you with monthly payouts for life. You can use your CPF savings to purchase a CPF LIFE plan at age 55.

How to Maximize Your CPF Withdrawal

To maximize your CPF withdrawal, consider the following tips:

- Contribute Regularly: Consistently contributing to your CPF account throughout your working life will increase your CPF balance and allow you to withdraw more in the future.

- Choose Wise Investments: The investment returns on your CPF savings can significantly impact your withdrawal amount. Select investment options that align with your risk tolerance and time horizon.

- Delay Withdrawal: If possible, consider delaying your CPF withdrawal to allow your savings to grow further and earn more interest.

- Consider a Top-up: If you have not contributed enough to your CPF, you can consider topping up your savings to reach the FRS amount and qualify for additional government subsidies.

Case Study: CPF Withdrawal Strategies

Let’s compare the CPF withdrawal strategies of two individuals:

Individual A: Withdrew the BRS amount of $93,000 at age 55.

Individual B: Delayed withdrawal until age 60 and accumulated an FRS amount of $186,000.

Individual B received a significantly higher CPF withdrawal amount despite having the same CPF balance at age 55. This demonstrates the importance of delaying withdrawal and letting your CPF savings grow over time.

Conclusion

Withdrawing CPF is a crucial decision that can impact your retirement security. Understanding the different withdrawal options, eligibility criteria, and factors that influence your withdrawal amount is essential for making informed decisions. By carefully considering these factors and adopting a strategic approach, you can maximize your CPF withdrawal and secure a comfortable retirement future.