Introduction

The Central Provident Fund (CPF) is a mandatory savings scheme in Singapore that helps citizens save for retirement, housing, and healthcare. CPF members can withdraw their savings when they reach a certain age or meet specific criteria.

In this article, we will provide a comprehensive guide on how much you can withdraw from CPF, including the different withdrawal options, withdrawal limits, and eligibility requirements.

CPF Withdrawal Options

There are two main ways to withdraw from CPF:

- CPF LIFE: CPF LIFE is a monthly payout scheme that provides members with a regular income for life.

- CPF Withdrawal Schemes: CPF withdrawal schemes allow members to withdraw their savings in lump sums or monthly installments.

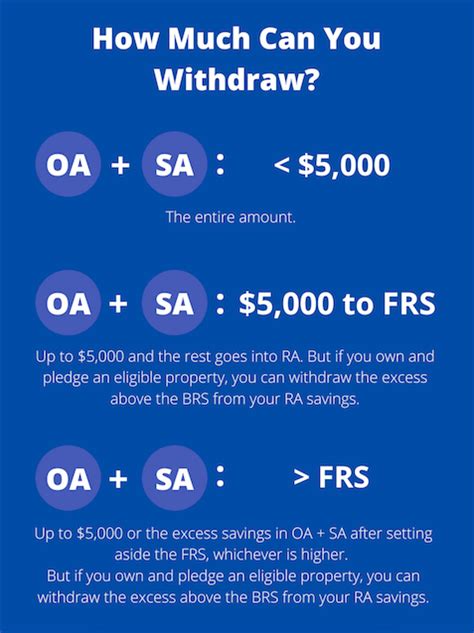

CPF Withdrawal Limits

The amount you can withdraw from CPF depends on your age, whether you have reached the CPF Minimum Sum, and your withdrawal option.

CPF LIFE:

- Basic Retirement Sum (BRS): The BRS is the minimum amount you need to have in your CPF account to qualify for CPF LIFE. The BRS is based on your age and is updated every year.

- Enhanced Retirement Sum (ERS): The ERS is a higher retirement sum that you can choose to save towards. If you have reached the ERS, you can withdraw up to 50% of your savings in a lump sum.

CPF Withdrawal Schemes:

- Full Retirement Sum (FRS): The FRS is the maximum amount you can withdraw from CPF when you reach the age of 55. The FRS is based on your age and is updated every year.

- Retirement Account (RA): The RA is a CPF account that you can use to save for retirement. You can withdraw up to 50% of your savings in a lump sum when you reach the age of 55.

Eligibility Requirements for CPF Withdrawal

To be eligible to withdraw from CPF, you must meet the following requirements:

- You must be a Singapore citizen or Permanent Resident.

- You must have reached the minimum withdrawal age (55 years old for CPF LIFE and 55 or 65 years old for CPF withdrawal schemes).

- You must have reached the CPF Minimum Sum (except for CPF LIFE).

How to Withdraw From CPF

You can withdraw from CPF online, at a CPF Service Centre, or through your bank.

Online:

- Go to the CPF website (https://www.cpf.gov.sg/).

- Log in to your CPF account.

- Click on the “Withdrawals” tab.

- Select the withdrawal option you want to use.

- Enter the amount you want to withdraw.

- Click on the “Submit” button.

CPF Service Centre:

- Go to a CPF Service Centre.

- Bring your NRIC and CPF statement.

- Fill out a withdrawal form.

- Submit the form to a CPF officer.

Bank:

- Go to a bank that offers CPF withdrawal services.

- Bring your NRIC and CPF statement.

- Fill out a withdrawal form.

- Submit the form to a bank teller.

Consequences of Withdrawing From CPF

Withdrawing from CPF early can have the following consequences:

- Lower retirement income

- Reduced healthcare coverage

- Penalties for withdrawing too much

Tips for Withdrawing From CPF

Here are a few tips for withdrawing from CPF:

- Consider your retirement needs before withdrawing.

- Withdraw only what you need.

- Consider using CPF LIFE to get a regular income for life.

- Seek professional advice if you are not sure how much to withdraw.

Conclusion

Withdrawing from CPF is a major financial decision. By understanding the different withdrawal options, withdrawal limits, and eligibility requirements, you can make informed decisions about how and when to withdraw from CPF.

Tables

Table 1: CPF Withdrawal Limits by Age

| Age | BRS | ERS | FRS |

|---|---|---|---|

| 55 | $93,000 | $289,000 | $186,000 |

| 56 | $96,000 | $304,000 | $192,000 |

| 57 | $99,000 | $319,000 | $198,000 |

| 58 | $103,000 | $335,000 | $204,000 |

| 59 | $107,000 | $351,000 | $210,000 |

Table 2: CPF Withdrawal Options

| Withdrawal Option | Minimum Age | Maximum Withdrawal |

|---|---|---|

| CPF LIFE | 55 | Up to 50% of ERS |

| CPF Withdrawal Schemes | 55 or 65 | Up to FRS |

Table 3: Eligibility Requirements for CPF Withdrawal

| Requirement | Details |

|---|---|

| Citizenship | Singapore citizen or Permanent Resident |

| Age | 55 years old for CPF LIFE, 55 or 65 years old for CPF withdrawal schemes |

| CPF Minimum Sum | Reached the CPF Minimum Sum (except for CPF LIFE) |

Table 4: Consequences of Withdrawing From CPF

| Consequence | Details |

|---|---|

| Lower retirement income | Reduced CPF savings will result in lower CPF LIFE payouts |

| Reduced healthcare coverage | CPF savings are used to fund MediSave, which provides healthcare coverage |

| Penalties for withdrawing too much | Penalties may be imposed if you withdraw more than the allowed limits |