Current Fixed Deposit Rates

As of May 2023, fixed deposit rates in Singapore have remained relatively stable, with minimal fluctuations compared to previous months. According to the Monetary Authority of Singapore (MAS), the average 12-month fixed deposit rate currently stands at 2.0%, while the average 24-month fixed deposit rate is 2.5%.

Historical Trends and Future Outlook

Historical Trends: Fixed deposit rates in Singapore have witnessed a gradual increase over the past year. In May 2022, the average 12-month fixed deposit rate was only 0.5%, while the average 24-month rate was 0.7%. This upward trend is primarily attributed to rising inflation and the subsequent tightening of monetary policy by the MAS.

Future Outlook: The future outlook for fixed deposit rates in Singapore remains uncertain. While rising inflation could continue to exert upward pressure on rates, the Singapore economy is expected to moderate in the coming months. This could lead to a gradual decline in fixed deposit rates towards the end of 2023.

Factors Affecting Fixed Deposit Rates

Numerous factors influence fixed deposit rates in Singapore, including:

- Inflation: Inflation is a major determinant of fixed deposit rates. When inflation rises, banks typically increase interest rates to maintain the real value of their deposits.

- Monetary Policy: The MAS plays a crucial role in setting interest rates and conducting monetary policy. When the MAS raises interest rates, banks tend to increase their fixed deposit rates accordingly.

- Market Competition: Fixed deposit rates are also influenced by competition among banks. In order to attract depositors, banks may offer higher rates, particularly during promotional periods.

- Economic Outlook: The overall economic outlook can also affect fixed deposit rates. In times of economic uncertainty, banks may lower rates to encourage saving and stabilize the financial system.

Choosing the Right Fixed Deposit Account

When selecting a fixed deposit account, several factors should be considered:

- Interest Rate: The interest rate is the most important factor to consider. Compare rates from different banks and choose the one that offers the highest return.

- Tenure: The tenure refers to the period of time for which the deposit will be locked in. Longer tenures typically offer slightly higher interest rates.

- Minimum Deposit: The minimum deposit required to open a fixed deposit account varies from bank to bank. Consider the minimum deposit amount and ensure it aligns with your financial capabilities.

- Fees and Charges: Some banks may impose fees and charges for opening a fixed deposit account or withdrawing funds before maturity. Be aware of these costs and compare them between banks.

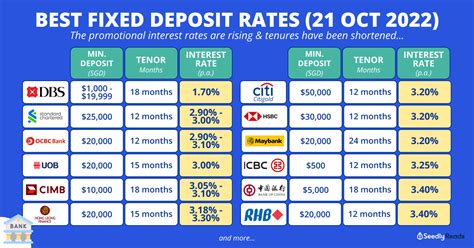

Table 1: Comparison of Fixed Deposit Rates in Singapore May 2023

| Bank | 12-Month Rate | 24-Month Rate |

|---|---|---|

| DBS Bank | 2.10% | 2.60% |

| OCBC Bank | 2.05% | 2.55% |

| UOB Bank | 2.00% | 2.50% |

| Standard Chartered Bank | 1.95% | 2.45% |

| Citibank | 1.90% | 2.40% |

Strategies for Maximizing Fixed Deposit Returns

Several strategies can be employed to maximize returns on fixed deposit accounts:

- Ladder Your Deposits: By distributing your deposits across multiple fixed deposit accounts with different maturities, you can lock in higher rates for longer periods and reduce the impact of interest rate fluctuations.

- Negotiate Higher Rates: If you have a substantial amount to deposit, you can negotiate a higher interest rate with the bank. This is especially effective for long-term fixed deposit accounts.

- Take Advantage of Promotional Offers: Banks often offer promotional rates for new customers or limited-time periods. Take advantage of these offers to secure higher returns.

- Consider Variable-Rate Fixed Deposits: Variable-rate fixed deposits allow you to benefit from potential interest rate increases while preserving the safety of your investment.

Pros and Cons of Fixed Deposit Accounts

Pros:

- Stable and Reliable Returns: Fixed deposit accounts offer a guaranteed rate of return, making them a reliable source of passive income.

- Low Risk: Fixed deposit accounts are considered low-risk investments, as the deposited funds are insured by the Singapore Deposit Insurance Corporation (SDIC) up to a certain amount.

- Convenience: Fixed deposit accounts can be opened and managed online or through mobile banking apps, making them highly convenient.

Cons:

- Locking in Rates: Fixed deposit accounts lock in the interest rate for a specific tenure. If interest rates rise significantly during this period, you may miss out on higher returns.

- Limited Flexibility: Funds in a fixed deposit account cannot be withdrawn before maturity without incurring penalties.

- Inflation Risk: Fixed deposit rates may not always keep pace with inflation, which can erode the real value of your returns over time.

FAQs

1. Are fixed deposit accounts safe?

Yes, fixed deposit accounts are considered safe investments as they are insured by the SDIC up to a certain amount.

2. What is the minimum deposit required for a fixed deposit account?

The minimum deposit required varies from bank to bank. Typically, it ranges from SGD 1,000 to SGD 5,000.

3. Can I withdraw funds from a fixed deposit account before maturity?

Yes, but it is generally not advisable. Withdrawing funds before maturity will result in a penalty and loss of interest.

4. How can I maximize my returns on fixed deposit accounts?

You can maximize your returns by laddering your deposits, negotiating higher rates, taking advantage of promotional offers, and considering variable-rate fixed deposits.

5. What are the risks associated with fixed deposit accounts?

The primary risks associated with fixed deposit accounts include locking in rates, limited flexibility, and inflation risk.

6. Is it a good idea to invest in fixed deposit accounts during high inflation?

Investing in fixed deposit accounts during high inflation may not be the best strategy, as the returns may not keep pace with rising prices.

7. What is the future outlook for fixed deposit rates in Singapore?

The future outlook for fixed deposit rates in Singapore is uncertain, but they may gradually decline towards the end of 2023 due to potential economic moderation.

8. Are there any alternatives to fixed deposit accounts?

There are alternative investment options such as bonds, treasury bills, and money market instruments that can provide similar returns to fixed deposit accounts.