The realm of health insurance has evolved drastically, offering a plethora of plans tailored to diverse needs. Two prominent players in this arena, Great Eastern Life and Supreme Health, stand out with their comprehensive offerings: Total Health and Supreme Health 2025. In this in-depth analysis, we delve into the intricacies of these two plans, uncovering their strengths, drawbacks, and which one might be the ideal fit for your health and financial goals.

Great Eastern Total Health: Unparalleled Flexibility and Customization

Great Eastern Total Health is renowned for its unparalleled flexibility, empowering policyholders to tailor their coverage based on their unique needs. With multiple plan options and customizable riders, you can craft a plan that perfectly aligns with your priorities.

Coverage Highlights:

- Comprehensive hospitalization coverage, including Cashless hospitalization at over 1,000 hospitals nationwide

- Extensive outpatient benefits, such as Specialist consultations, Day surgeries and Dental treatments

- Preventive health screenings and wellness programs to promote overall well-being

- Optional riders to enhance coverage for critical illnesses, long-term care, and more

Premiums and Deductibles:

Premiums for Great Eastern Total Health vary depending on factors such as age, health status, and coverage level. Deductibles, a fixed amount you pay before coverage kicks in, range from RM500 to RM5,000.

Advantages:

- Customization: Unmatched ability to customize coverage based on specific needs and budget.

- Rider Flexibility: Wide range of optional riders to supplement coverage and address unique concerns.

- Wellness Programs: Focus on preventive health and well-being, empowering policyholders to take an active role in their health.

Disadvantages:

- Higher Premiums: Premiums can be higher compared to standardized plans due to the level of customization.

- Deductibles: Deductibles may apply for certain benefits, potentially increasing out-of-pocket expenses.

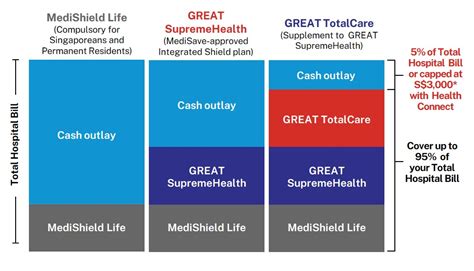

Supreme Health 2025: Enhanced Coverage with a Future-Forward Vision

Supreme Health 2025 is a premium health insurance plan designed to meet the evolving healthcare landscape. It boasts comprehensive coverage, innovative features, and a focus on long-term health management.

Coverage Highlights:

- In-patient and out-patient coverage for a wide range of medical expenses

- Unlimited lifetime coverage for specified critical illnesses

- Comprehensive cancer coverage, including coverage for early-stage and advanced-stage cancer

- Access to stem cell therapy for eligible conditions

- Telemedicine services for convenient consultations and prescription refills

Premiums and Deductibles:

Supreme Health 2025 premiums are fixed based on age and coverage level. There is no deductible applied to the plan.

Advantages:

- Enhanced Coverage: Extensive coverage for critical illnesses, cancer, and advanced medical treatments.

- Unlimited Lifetime Coverage: Peace of mind with lifetime coverage for specified critical illnesses.

- Innovative Features: Embraces technological advancements like telemedicine and stem cell therapy.

- No Deductibles: Simplified coverage without the burden of deductibles.

Disadvantages:

- Higher Premiums: Premiums are typically higher compared to traditional health insurance plans.

- Limited Customization: Coverage is standardized, offering less flexibility compared to customizable plans.

Great Eastern Total Health vs. Supreme Health 2025: Which One is Right for You?

The choice between Great Eastern Total Health and Supreme Health 2025 depends on your individual circumstances and priorities.

- If you prioritize customization and flexibility: Great Eastern Total Health offers unmatched flexibility to tailor your coverage and budget.

- If you seek comprehensive coverage and innovative features: Supreme Health 2025 provides enhanced protection against critical illnesses, cancer, and future healthcare advancements.

Tips and Tricks for Choosing the Right Health Insurance Plan

- Assess Your Healthcare Needs: Determine the level of coverage and benefits you require based on your medical history, family history, and lifestyle.

- Compare Coverage and Premiums: Carefully review the coverage details and premium structures of different plans to identify the most suitable option.

- Consider Rider Flexibility: Explore optional riders that can supplement coverage and address specific concerns.

- Seek Professional Advice: Consult with an insurance agent or financial advisor to gain insights and guidance on selecting the right plan for your needs.

FAQs:

1. What is the difference between a deductible and a co-pay?

A deductible is a fixed amount you pay out-of-pocket before coverage kicks in. A co-pay, on the other hand, is a fixed amount you pay for specific services, such as doctor’s visits or prescription drugs.

2. Are there any age restrictions for health insurance plans?

Most health insurance plans have age restrictions, typically covering individuals between the ages of 18 and 65. However, some plans may offer extended coverage for seniors or children.

3. Can I switch health insurance plans if I am not satisfied with my current one?

Yes, you can switch health insurance plans during the open enrollment period or if you experience a qualifying life event, such as marriage or the birth of a child.

4. What is a preexisting condition?

A preexisting condition is a medical condition that you had before enrolling in a health insurance plan. Some plans may exclude coverage for preexisting conditions or impose waiting periods.

5. What are the benefits of telemedicine services?

Telemedicine services allow you to consult with healthcare providers remotely, offering convenience, accessibility, and reduced travel costs.

6. Is it important to review my health insurance coverage regularly?

Yes, it is important to review your health insurance coverage regularly to ensure that it still meets your evolving needs and circumstances.

7. Can I contribute additional funds to my health savings account (HSA)?

Yes, you can contribute additional funds to your HSA if you have an eligible high-deductible health plan (HDHP). The contributed funds grow tax-free and can be used for qualified medical expenses.

8. What is the role of a health insurance agent?

A health insurance agent can provide personalized guidance, compare different plans, and help you select the coverage that best aligns with your needs and budget.