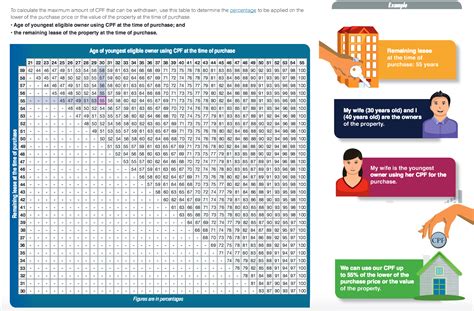

Estimate Your CPF Usage with Our Comprehensive Guide

Purchasing a property with a leasehold tenure of less than 60 years comes with unique considerations. One crucial aspect is determining the amount of Central Provident Fund (CPF) you can utilize for this purpose. Our comprehensive CPF calculator and guide will help you navigate this process seamlessly.

Key Considerations for CPF Withdrawal

- Lease Duration: The CPF withdrawal limit is based on the remaining lease tenure and the property’s estimated value.

- Property Value: The higher the property value, the more CPF you can withdraw.

- Age and Citizenship: Your age and citizenship status influence the CPF withdrawal limits.

CPF Calculator for Property Less Than 60 Years Lease

Our user-friendly CPF calculator simplifies the process of estimating your CPF withdrawal for a property with a leasehold tenure of less than 60 years. Simply input the following information:

- Purchase Price

- Remaining Lease Tenure

- Estimated Property Value

- Age

- Citizenship Status

The calculator will provide you with an approximate amount of CPF you can withdraw.

Withdrawal Limits: A Comprehensive Overview

According to the Central Provident Fund Board (CPF Board), the withdrawal limits for properties with leaseholds less than 60 years are as follows:

| Lease Tenure | Withdrawal Limit |

|---|---|

| 60 to 50 years | Up to 80% of CPF funds |

| 49 to 40 years | Up to 75% of CPF funds |

| 39 to 30 years | Up to 70% of CPF funds |

| 29 to 20 years | Up to 65% of CPF funds |

| 19 to 10 years | Up to 60% of CPF funds |

| Less than 10 years | Up to 50% of CPF funds |

Additional Considerations

- Maximum CPF Withdrawal Amount: The maximum amount you can withdraw from your CPF account for property purchase is S$50,000 or 120% of your annual salary, whichever is lower.

- First-Time Homebuyers: First-time homebuyers are eligible for an additional CPF housing grant of up to S$15,000.

- Resale Levy: If you are purchasing a resale property, you may be subject to a resale levy, which will reduce the amount of CPF you can withdraw.

Tips for Maximizing CPF Withdrawal

- Consider purchasing a property with a longer remaining lease tenure.

- Explore options for leasehold extension to increase the value of your CPF withdrawal.

- Make sure to have sufficient CPF funds available to meet the withdrawal limits.

- Consult with a CPF advisor to tailor the withdrawal strategy to your specific needs.

Conclusion

Purchasing a property with a leasehold tenure of less than 60 years can be a savvy investment with careful planning. By leveraging our CPF calculator and understanding the withdrawal limits, you can confidently estimate your CPF usage and make an informed decision. Remember to consult with a CPF advisor or visit the CPF website for further guidance.

Tables

| Property Value | CPF Withdrawal Limit (Based on 60-Year Lease) |

|---|---|

| S$100,000 | S$80,000 |

| S$200,000 | S$160,000 |

| S$300,000 | S$240,000 |

| S$400,000 | S$320,000 |

| S$500,000 | S$400,000 |

| Age | CPF Withdrawal Limit |

|---|---|

| 30 years old | Up to 80% |

| 40 years old | Up to 75% |

| 50 years old | Up to 70% |

| 60 years old | Up to 65% |

| 70 years old | Up to 60% |

| Citizenship Status | CPF Withdrawal Limit |

|---|---|

| Singapore Citizen | Up to 100% |

| Singapore Permanent Resident (SPR) | Up to 80% |

| Non-Resident | Up to 50% |

| Lease Tenure | Estimated Property Value | CPF Withdrawal Limit |

|---|---|---|

| 55 years | S$400,000 | S$280,000 |

| 45 years | S$300,000 | S$210,000 |

| 35 years | S$200,000 | S$140,000 |

| 25 years | S$100,000 | S$70,000 |

| 15 years | S$50,000 | S$35,000 |