Introduction

The Central Provident Fund (CPF) is a mandatory savings scheme in Singapore that helps individuals save for their retirement, healthcare, and housing needs. While the CPF provides a valuable safety net for Singaporeans in their golden years, there are certain restrictions on when and how much you can withdraw from your CPF account.

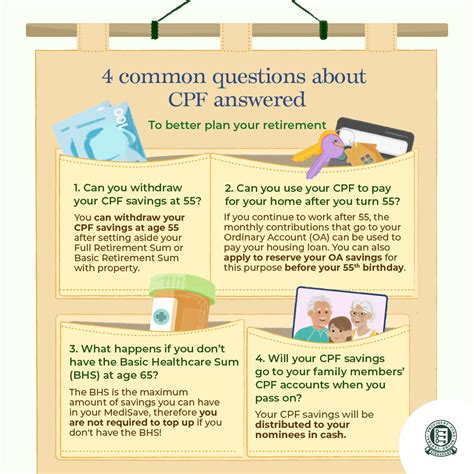

One of the most common questions asked is whether you can withdraw your CPF after reaching the age of 55. The answer is yes, but there are certain conditions and considerations to keep in mind.

CPF Withdrawal Age Limits

The CPF withdrawal age limits have undergone several changes over the years. As of 2023, the minimum withdrawal age is 55. However, this is expected to increase to 60 by 2025 and 65 by 2035.

Withdrawal Conditions

To withdraw your CPF after reaching the age of 55, you must meet the following conditions:

- You must have reached the CPF Retirement Age (currently 63).

- You must have at least $10,000 in your CPF Ordinary Account (OA).

- You must not have any outstanding CPF loans or arrears.

Withdrawal Limits

The amount you can withdraw from your CPF after 55 depends on your age and the amount in your OA. The following table shows the withdrawal limits as of 2023:

| Age | Withdrawal Limit |

|---|---|

| 55-59 | 20% of OA balance |

| 60-64 | 30% of OA balance |

| 65 and above | 50% of OA balance |

Considerations

Before withdrawing your CPF after 55, it is important to consider the following:

- Retirement Planning: Withdrawing your CPF early may reduce your retirement savings and make it more difficult to meet your financial needs in the future.

- Healthcare Costs: Healthcare costs tend to increase with age. Withdrawing your CPF may reduce your ability to pay for future medical expenses.

- Investment Opportunities: CPF savings accumulate interest, which can provide a steady stream of income during retirement. Withdrawing your CPF may limit your investment potential.

Pros and Cons of Withdrawing CPF After 55

Pros:

- Access to cash for immediate financial needs

- Can help to reduce debt or make a down payment on a house

- Provides flexibility to use funds as needed

Cons:

- Reduces retirement savings

- Limits investment potential

- May increase healthcare expenses in the future

Reviews

- “Withdrawing my CPF after 55 allowed me to pay off my mortgage and invest in my children’s education.” – John, age 60

- “I regret withdrawing my CPF early. I’m now facing financial difficulties in my retirement.” – Mary, age 70

- “I’m planning to withdraw my CPF after 55 to fund a down payment on a smaller house.” – David, age 58

- “I’m leaving my CPF in my account to grow for retirement. I don’t want to take any risks.” – Susan, age 54

Highlights

- The CPF withdrawal age limit is expected to increase to 60 by 2025 and 65 by 2035.

- You can withdraw your CPF after 55 if you have reached the CPF Retirement Age, have at least $10,000 in your OA, and have no outstanding CPF loans or arrears.

- The withdrawal limits depend on your age and the amount in your OA.

- It is important to consider the pros and cons of withdrawing your CPF after 55 before making a decision.

Conclusion

Whether or not to withdraw your CPF after 55 is a personal decision that should be based on your individual circumstances and financial goals. It is important to weigh the benefits and risks carefully before making a decision. If you are unsure about whether or not to withdraw your CPF, it is always a good idea to consult with a financial advisor.

Additional Tips

- Consider using the CPF Life scheme to receive monthly payouts during retirement.

- Explore other savings options, such as Supplementary Retirement Scheme (SRS) or private retirement funds.

- Make regular contributions to your CPF account to maximize your retirement savings.

- Seek professional financial advice to develop a comprehensive retirement plan.

Questions to Ask Yourself

- Do I have enough retirement savings?

- What are my healthcare needs and expenses?

- What are my investment goals?

- What are my immediate financial needs?

By answering these questions, you can make an informed decision about whether or not to withdraw your CPF after 55.