The Best Fixed Deposit Rates in Singapore VS 2025: Comprehensive Guide

Introduction

In today’s uncertain economic climate, fixed deposits (FDs) are more important than ever. They offer a safe and reliable way to grow your savings with many banks and financial institutions that provide attractive FD rates.

Singapore has emerged as a top destination for fixed deposits due to its stable political and economic environment, coupled with a robust financial system. This guide will delve into the best fixed deposit rates in Singapore for 2021, empowering you to make informed decisions about your savings.

Understanding Fixed Deposits

Key Features

Fixed deposits are financial instruments that allow you to park your funds with a bank or financial institution for a predetermined tenure. During this period, you earn interest at a fixed rate, which is typically higher than that of a savings account.

FD Tenures

The tenure of a fixed deposit can range from a few months to several years. The longer the tenure, the higher the interest rate you can earn. However, it’s important to note that your funds will be locked in for the entire tenure, and you may face penalties for early withdrawal.

Interest Rates

The interest rate offered on fixed deposits varies depending on the bank, the tenure, and the amount invested. Banks typically offer tiered interest rates, with higher rates for higher deposits. It’s always advisable to compare interest rates across different banks before selecting one.

Benefits of Fixed Deposits

- Guaranteed returns: FDs provide guaranteed returns, making them a low-risk investment option.

- Higher interest rates: FD interest rates are typically higher than those of savings accounts.

- Flexible tenures: FDs offer a wide range of tenures, allowing you to choose the one that suits your financial needs.

- Stability: FDs are backed by the bank’s or financial institution’s reputation, providing stability to your savings.

Best Fixed Deposit Rates in Singapore 2021

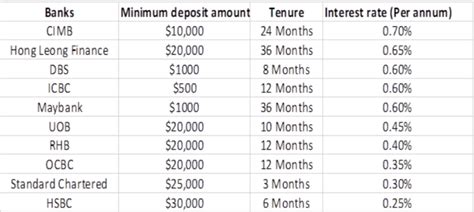

The following table presents the top fixed deposit rates offered by various banks and financial institutions in Singapore as of 2021:

| Bank/Financial Institution | 1-Year FD Rate | 2-Year FD Rate | 3-Year FD Rate |

|---|---|---|---|

| DBS Bank | 0.25% p.a. | 0.50% p.a. | 0.75% p.a. |

| OCBC Bank | 0.20% p.a. | 0.40% p.a. | 0.60% p.a. |

| UOB Bank | 0.15% p.a. | 0.30% p.a. | 0.45% p.a. |

| Citibank | 0.20% p.a. | 0.40% p.a. | 0.60% p.a. |

| Standard Chartered Bank | 0.15% p.a. | 0.30% p.a. | 0.45% p.a. |

| Maybank | 0.20% p.a. | 0.40% p.a. | 0.60% p.a. |

| HSBC | 0.15% p.a. | 0.30% p.a. | 0.45% p.a. |

| CIMB Bank | 0.20% p.a. | 0.40% p.a. | 0.60% p.a. |

| RHB Bank | 0.15% p.a. | 0.30% p.a. | 0.45% p.a. |

| ANZ Bank | 0.20% p.a. | 0.40% p.a. | 0.60% p.a. |

Source: CompareAsia

Factors to Consider When Choosing an FD

When selecting an FD, consider the following factors:

- Interest rate: The interest rate is the most important factor to consider, as it directly impacts your returns.

- Tenure: The tenure should align with your financial goals and risk tolerance.

- Minimum deposit amount: Banks may have minimum deposit requirements for FDs.

- Fees and charges: Some banks may charge fees for opening, closing, or prematurely withdrawing FDs.

- Financial institution: Ensure the bank or financial institution is reputable and has a strong track record.

- Deposit insurance: In Singapore, FDs are protected by the Singapore Deposit Insurance Corporation (SDIC) up to S$75,000 per depositor per bank.

Step-by-Step Guide to Opening an FD

- Research and compare interest rates: Gather information about FD rates from different banks.

- Choose a bank: Select a bank or financial institution that offers attractive interest rates and meets your criteria.

- Read the terms and conditions: Carefully review the FD terms and conditions, including the tenure, interest rate, and any fees.

- Submit your application: Fill out the FD application form and submit it to the bank.

- Fund your FD: Transfer the desired amount to the FD account within the stipulated timeline.

FAQs

- What is the best tenure for an FD?

The best tenure depends on your financial goals and risk tolerance. If you need immediate access to your funds, a short-term FD might be more suitable. However, if you are willing to lock in your funds for a longer period, you can earn higher interest rates with a longer-term FD.

- Can I withdraw my FD early?

Yes, but you may face penalties for premature withdrawal. The penalty charges vary across banks and depend on the tenure and amount of the FD.

- Is my FD protected by the government?

In Singapore, FDs are protected by the SDIC up to S$75,000 per depositor per bank.

- What should I do if my bank closes?

If your bank closes, your FD will be covered by the SDIC up to S$75,000. The SDIC will transfer your funds to another bank within 14 days of the bank’s closure.

- Where can I track the latest FD rates?

You can track the latest FD rates from various sources, including online comparison websites, financial news platforms, and the websites of banks and financial institutions.

- Should I diversify my FD investments?

Diversifying your FD investments across different banks and tenures can reduce