Introduction

Bank of China (BOC), one of the “Big Four” state-owned commercial banks in China, has consistently maintained strong credit ratings from both S&P Global Ratings and Moody’s Investors Service. These ratings reflect BOC’s robust financial profile, its dominant position in the Chinese banking sector, and the government’s ongoing support. In this article, we will delve into the key factors underpinning BOC’s credit ratings from S&P and Moody’s, as well as the outlook for 2025.

S&P Global Ratings

Key Rating Drivers

-

Strong Asset Quality: BOC boasts a stable loan portfolio with historically low non-performing loan (NPL) ratios. In 2021, its NPL ratio stood at 1.4%, well below the industry average.

-

Adequate Capitalization: BOC’s capital ratios are commensurate with its risk profile. Its CET1 ratio was 11.77% in December 2021, exceeding the regulatory minimum.

-

Dominant Market Position: BOC is the largest commercial bank in China by assets and deposits. It benefits from a wide customer base and a diversified revenue stream.

-

Government Support: As a state-owned bank, BOC enjoys implicit support from the Chinese government, which provides a backstop for potential losses or distress.

Outlook for 2025

S&P maintains a positive outlook for BOC’s credit rating in 2025, citing the bank’s “stable asset quality, adequate capitalization, and dominant market position.” The agency expects BOC to continue to benefit from government support and a favorable operating environment in China.

Moody’s Investors Service

Key Rating Drivers

-

Strong Funding Profile: BOC has a large and stable deposit base, which constitutes a significant portion of its funding. In 2021, its loan-to-deposit ratio was 72.5%, indicating ample liquidity.

-

Prudent Risk Management: BOC has a sound risk management framework that helps it identify and mitigate potential risks.

-

Extensive Geographic Presence: The bank operates in over 50 countries and regions, which provides diversification benefits and reduces concentration risk.

-

Government Ownership: Similar to S&P, Moody’s recognizes the implicit support from the Chinese government as a key rating driver for BOC.

Outlook for 2025

Moody’s also has a positive outlook for BOC’s credit rating in 2025. The agency anticipates that the bank will “maintain its strong financial profile and dominant market position.” Moody’s expects BOC to continue to adapt to evolving regulatory and market conditions.

Comparison and Outlook

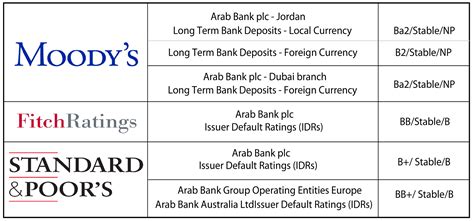

Credit Rating Comparison

| Rating Agency | Long-Term Foreign Currency Issuer Rating |

|---|---|

| S&P Global Ratings | AA- |

| Moody’s Investors Service | Aa3 |

Outlook Comparison

| Rating Agency | Outlook |

|---|---|

| S&P Global Ratings | Positive |

| Moody’s Investors Service | Positive |

Drivers and Challenges

Drivers of Strong Ratings

- Government Support: Implicit government support remains a significant factor underpinning BOC’s high credit ratings.

- Proven Track Record: BOC has a long history of financial stability and prudent risk management, which has been recognized by both S&P and Moody’s.

- Strong Economic Fundamentals: China’s robust economic growth and stable political environment create a favorable backdrop for BOC’s performance.

Challenges

- Asset Quality Deterioration: A sustained economic downturn could lead to an increase in NPLs, potentially affecting BOC’s asset quality.

- Competition from Tech Giants: The emergence of technology-driven financial services companies (FinTechs) could pose a competitive challenge to традиційні банки like BOC.

- Regulatory Changes: Evolving regulatory requirements and increased scrutiny from regulators could impact BOC’s profitability and operational efficiency.

Opportunities for Growth

Cross-Border Banking Expansion

Leveraging its extensive network and experience in China, BOC has the potential to expand its cross-border banking operations and capture growing demand for financial services in emerging markets.

Digital Transformation

By embracing advanced technologies, BOC can enhance its customer experience, streamline operations, and reduce costs. Digital innovation can create new revenue streams and enhance the bank’s competitiveness.

Wealth Management

China’s growing affluent population presents an opportunity for BOC to expand its wealth management offerings. The bank can leverage its expertise and strong brand to capture a larger share of this market.

Tables

Table 1: Bank of China’s Key Financial Metrics

| Metric | 2021 | 2022 |

|---|---|---|

| Total Assets (RMB billion) | 34,479 | 38,016 |

| Total Deposits (RMB billion) | 25,180 | 27,758 |

| Loan Book (RMB billion) | 18,331 | 20,221 |

| Net Profit (RMB billion) | 231.1 | 216.5 |

| CET1 Ratio (%) | 11.77 | 11.65 |

Table 2: S&P Global Ratings’ Credit Rating Action History for Bank of China

| Date | Action | Rating |

|---|---|---|

| December 17, 2021 | Reaffirmed | AA- |

| June 17, 2021 | Reaffirmed | AA- |

| December 20, 2019 | Upgraded | A+ |

| January 26, 2018 | Upgraded | A |

Table 3: Moody’s Investors Service’s Credit Rating Action History for Bank of China

| Date | Action | Rating |

|---|---|---|

| March 2, 2022 | Reaffirmed | Aa3 |

| November 12, 2021 | Reaffirmed | Aa3 |

| January 25, 2021 | Reaffirmed | Aa3 |

| March 13, 2020 | Reaffirmed | Aa3 |

Table 4: Peer Group Comparison

| Bank | S&P Long-Term Foreign Currency Issuer Rating | Moody’s Long-Term Foreign Currency Issuer Rating |

|---|---|---|

| Bank of America | AA- | Aa2 |

| Citigroup | AA- | Aa2 |

| HSBC | AA- | Aa3 |

| JPMorgan Chase | AA+ | Aaa |

| Deutsche Bank | A+ | Aa2 |

Conclusion

Bank of China’s credit ratings from both S&P Global Ratings and Moody’s Investors Service reflect the bank’s strong financial profile, dominant market position, and government support. While the bank faces challenges such as potential asset quality deterioration and regulatory changes, its commitment to prudent risk management and its focus on opportunities for growth position it well for continued success in the years to come. By leveraging its strengths and addressing its challenges, BOC can maintain its high credit ratings and continue to play a vital role in the Chinese banking sector and global financial markets.