Introduction

The Central Provident Fund (CPF) is a mandatory savings scheme in Singapore that helps individuals accumulate funds for retirement, healthcare, and housing. At the age of 55, CPF members face important decisions regarding the management of their CPF savings. This article explores the changes that occur to CPF at age 55 and compares the different options available to members in 2025.

CPF Balances at 55

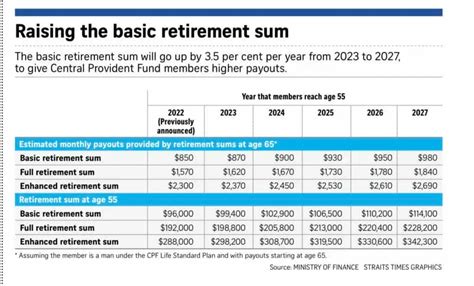

According to the CPF Board, the median CPF balance for members turning 55 in 2025 is projected to be $250,000, an increase from the current median balance of $220,000. This growth is attributed to factors such as increased contributions, higher returns on CPF investments, and the expansion of CPF schemes.

Key Changes at 55

Upon reaching age 55, CPF members experience several key changes:

- Automatic Transfer to Retirement Account (RA)

-

50% of the Ordinary Account (OA) balance is transferred to the RA, subject to a maximum of $142,900.

-

Lifelong CPF Income Scheme (CPF LIFE)

- CPF members can now opt into CPF LIFE, a government scheme that provides monthly payouts for life. The minimum entry age for CPF LIFE will be gradually raised to 65 by 2035.

Options for CPF Savings

At 55, CPF members have the following options for their CPF savings:

Table 1: CPF Withdrawal Options at 55

| Option | Description |

|---|---|

| Full Withdrawal | Withdraw all CPF savings, including OA, SA, and MA balances. |

| CPF LIFE | Receive monthly payouts for life, supported by annuity purchases. |

| CPF LIFE Eshield | Similar to CPF LIFE, but with a guaranteed payout period of 20 years. |

| Deferred Withdrawal | Postpone CPF withdrawal until a later age, earning additional interest on CPF savings. |

| Property Purchase | Use CPF savings to purchase a property for residential or investment purposes. |

Choosing the Right Option

The best option for your CPF savings depends on your individual circumstances and retirement needs. Consider factors such as:

- Retirement income goals

- Health and life expectancy

- Housing arrangements

- Risk tolerance

- Tax implications

Advantages and Disadvantages

Table 2: Advantages and Disadvantages of CPF Withdrawal Options

| Option | Advantages | Disadvantages |

|---|---|---|

| Full Withdrawal | Instant access to funds | Loss of potential earnings and retirement income |

| CPF LIFE | Regular monthly income | Lower returns than other investment options |

| CPF LIFE Eshield | Guaranteed payout period | Higher monthly payouts than CPF LIFE |

| Deferred Withdrawal | Higher interest earnings | Delayed access to funds |

| Property Purchase | Potential for capital gains | Mortgage expenses and property maintenance costs |

CPF Withdrawal Limit

The CPF withdrawal limit at 55 is based on a combination of factors, including the member’s age, citizenship status, and housing type.

Table 3: CPF Withdrawal Limits at 55

| Category | Withdrawal Limit |

|---|---|

| Singapore Citizen with HDB Property | 25% of OA balance |

| Singapore Citizen with Non-HDB Property | 50% of OA balance |

| Permanent Resident with HDB Property | 25% of OA balance |

| Permanent Resident with Non-HDB Property | 50% of OA balance |

| Foreigner with HDB Property | 50% of OA balance |

| Foreigner with Non-HDB Property | 100% of OA balance |

Conclusion

At the age of 55, CPF members enter a crucial phase in their financial planning. With the changes to CPF balances, options, and withdrawal limits, it is essential to carefully consider the best strategy for managing retirement savings. By understanding the options available and seeking professional advice if needed, individuals can make informed decisions that will secure their financial well-being in the years to come.