Introduction

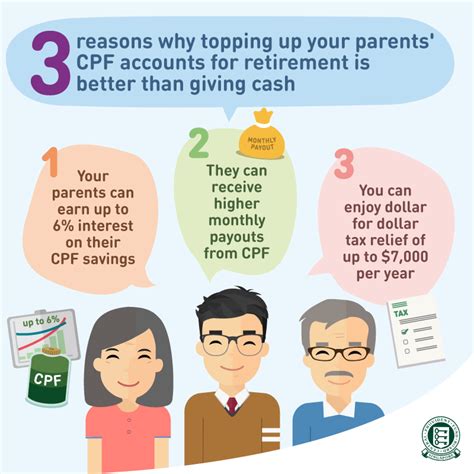

Supporting our elderly parents is a key aspect of filial piety. One way to ensure their financial well-being is to top up their Central Provident Fund (CPF) accounts. With the government introducing new enhancements in 2025, it has become more beneficial than ever to consider topping up your parents’ CPF.

Benefits of Topping Up CPF

The CPF is a retirement savings plan that provides several benefits to its members:

- Higher Retirement Income: CPF savings earn interest, which compounds over time to provide a higher retirement income.

- Tax Relief: Contributions to the CPF are tax-deductible, reducing your taxable income.

- Housing Grants: CPF savings can be used to purchase a home or pay for housing upgrades.

- Healthcare Expenses: CPF savings can be used to pay for healthcare expenses, including nursing home fees.

Eligibility for CPF Top-Ups

To be eligible to top up your parents’ CPF, they must meet the following criteria:

- Singapore Citizens or Permanent Residents: Your parents must be Singapore citizens or permanent residents.

- Age: They must be at least 55 years old.

- CPF Contribution Ceiling: Their current CPF balances and top-ups must not exceed the contribution ceilings.

How to Top Up Parents’ CPF

There are two options for topping up your parents’ CPF:

- Cash Top-Up: You can make cash contributions directly to your parents’ CPF accounts through the CPF Member Portal or any CPF Service Centre.

- Employer Top-Up: If your parents are still working, you can request your employer to make Special Employment Contributions (SECs) on their behalf.

2025 Enhancements to CPF Top-Ups

The government has introduced several enhancements to CPF top-ups that will take effect from 2025:

- Higher Tax Relief Cap: The tax relief cap for cash top-ups will be increased from $7,000 to $14,000 per year.

- Additional Matching Grant: The government will provide an additional matching grant of up to $6,000 per year for cash top-ups made to eligible parents.

- Lower Minimum Age for Matching Grant: The minimum age for receiving the matching grant will be lowered from 65 to 55 years old.

Step-by-Step Guide to Top-Ups

- Check Eligibility: Confirm that your parents meet the eligibility criteria for CPF top-ups.

- Determine Top-Up Amount: Consider your parents’ financial situation and needs to determine the appropriate top-up amount.

- Choose Top-Up Method: Decide whether to make a cash top-up or request an employer top-up.

- Make the Top-Up: Follow the instructions provided by the CPF Board or your employer to make the top-up contribution.

- Claim Tax Relief: If you made a cash top-up, remember to claim tax relief when filing your income tax return.

Pain Points and Motivations for Top-Ups

Pain Points:

- Insufficient Retirement Savings: Many elderly individuals have inadequate retirement savings due to limited earning capacity or unforeseen expenses.

- Rising Healthcare Costs: The cost of healthcare is rising rapidly, putting a strain on seniors’ finances.

- Inflation: Inflation erodes the value of retirement savings, making it difficult for seniors to maintain their standard of living.

Motivations:

- Provide Financial Stability: CPF top-ups can help ensure that your parents have a secure financial foundation in their retirement years.

- Reduce Healthcare Costs: CPF savings can be used to pay for healthcare expenses, reducing the financial burden on seniors and their families.

- Protect Against Inflation: The interest earned on CPF savings can help offset the effects of inflation and preserve the value of your parents’ retirement savings.

Stand Out: Innovation in CPF Top-Ups

To stand out in the competitive landscape of retirement planning, financial institutions can consider innovative approaches to CPF top-ups:

- Personalized Top-Up Recommendations: Utilize data analytics to provide customized top-up recommendations based on individuals’ financial profiles and retirement goals.

- Digital Platforms: Develop user-friendly digital platforms that make it easy for individuals to top up their parents’ CPF accounts remotely.

- Gamification: Introduce gamification elements to make CPF top-ups more engaging and rewarding for users.

Conclusion

Topping up your parents’ CPF is a thoughtful gesture that can significantly enhance their financial well-being in retirement. With the 2025 enhancements, it is now more advantageous than ever to consider this option. By understanding the benefits, eligibility, and step-by-step process, you can help ensure that your parents have a secure financial future.