Table of Contents

- Fixed Deposit Rates in Singapore

- How to Choose the Best Fixed Deposit Rate

- Benefits of Fixed Deposits

- Tips and Tricks for Maximizing Your Returns

- Common Mistakes to Avoid

- Future Trends in Fixed Deposits

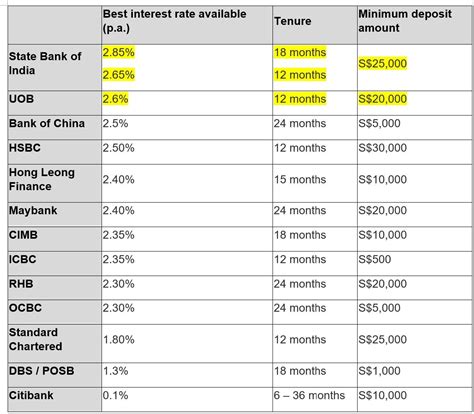

1. Fixed Deposit Rates in Singapore

| Bank | 1-Year Fixed Deposit Rate** | 2-Year Fixed Deposit Rate** |

|---|---|---|

| DBS Bank | 2.00% | 2.50% |

| OCBC Bank | 2.10% | 2.60% |

| UOB Bank | 2.20% | 2.70% |

| Citibank Singapore | 2.25% | 2.75% |

| Standard Chartered Bank | 2.30% | 2.80% |

2. How to Choose the Best Fixed Deposit Rate

Consider the following factors when choosing a fixed deposit rate:

- Duration: Determine the period you wish to lock in your funds.

- Amount: Different banks may offer varying rates depending on the deposit amount.

- Renewal options: Check if the fixed deposit can be automatically renewed at maturity.

- Interest payout: Decide whether you prefer regular interest payments or a lump sum at maturity.

- Fees and charges: Inquire about any associated fees or charges.

3. Benefits of Fixed Deposits

- Guaranteed returns: Unlike investments like stocks, fixed deposits provide a guaranteed rate of return.

- Low risk: Fixed deposits are considered a low-risk investment option.

- Tax-free interest: Interest earned on fixed deposits up to S$10,000 per year is tax-free in Singapore.

- Emergency fund: Fixed deposits can serve as an emergency fund for unexpected expenses.

- Diversification: Fixed deposits can diversify your investment portfolio and reduce overall risk.

4. Tips and Tricks for Maximizing Your Returns

- Compare rates: Shop around and compare rates offered by different banks.

- Negotiate: Contact the bank to negotiate a higher rate, especially if you are depositing a large amount.

- Consider a laddered approach: Spread your investment across multiple fixed deposits with varying maturity dates to mitigate interest rate fluctuations.

- Take advantage of promotions: Look out for promotional rates offered by banks.

- Round up your deposit amount: A slightly higher deposit amount can lead to a higher interest rate.

5. Common Mistakes to Avoid

- Choosing a low rate: Don’t settle for the first rate you come across. Compare and negotiate to maximize your returns.

- Breaking the fixed deposit term: This may result in penalties and loss of interest.

- Depositing all your savings: Diversify your investments and don’t put all your eggs in one basket.

- Not considering tax implications: Ensure you understand the tax implications of interest earned on fixed deposits.

- Overlooking fees and charges: Be aware of any associated fees or charges that may reduce your returns.

6. Future Trends in Fixed Deposits

- Digitalization: Banks are increasingly offering online fixed deposit services for convenience and efficiency.

- Customization: Fixed deposits may become more customizable, allowing investors to tailor rates and terms to their specific needs.

- Higher rates: As interest rates rise, fixed deposit rates are expected to follow suit.

- Sustainability-linked: Banks may offer fixed deposits that are linked to sustainability initiatives, providing investors with an opportunity to contribute to green initiatives while earning returns.

- FDs as an alternative to bonds: Fixed deposits could become a more attractive alternative to bonds due to their simplicity and guaranteed returns.

Conclusion

Fixed deposits continue to play a vital role in Singapore’s investment landscape, offering guaranteed returns and low risk. By following these tips and staying informed about future trends, you can maximize your returns and secure your financial future.