Understanding Employer CPF Contribution (ECPF)

The Central Provident Fund (CPF) is a mandatory social security savings scheme in Singapore that helps individuals build a retirement fund, healthcare expenses, and housing needs. Employers are required to contribute a portion of their employees’ salaries to the CPF, which is known as Employer CPF Contribution (ECPF).

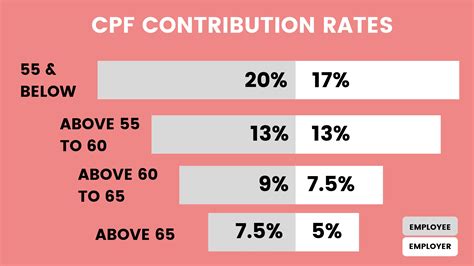

Current ECPF Rates

As of 2023, the ECPF rates are as follows:

- Ordinary Account (OA): 17%

- Special Account (SA): 9%

- Medisave Account (MA): 7%

Contribution Limits

ECPF contributions are subject to a monthly wage limit. For 2023, the monthly wage ceiling for ECPF contributions is S$6,000. This means that employers are only required to contribute ECPF on the first S$6,000 of an employee’s salary.

Benefits of ECPF for Employers

- Employee Retention: ECPF contributions can enhance employee loyalty and retention, as they provide a sense of financial security and retirement planning.

- Tax Savings: ECPF contributions are tax-deductible for employers, reducing their corporate income tax liability.

- Improved Employee Well-being: ECPF contributions support employees’ financial stability and well-being, ultimately benefiting the overall productivity and performance of the organization.

Strategies for Optimizing ECPF Contributions

- Provide Flexible CPF Contribution Plans: Allow employees to choose the proportion of their CPF contributions between their OA, SA, and MA accounts.

- Offer Supplementary Retirement Plans: Consider establishing additional retirement savings plans to complement ECPF contributions.

- Enhance Employee Financial Education: Educate employees about the benefits and implications of CPF contributions and long-term financial planning.

Tips and Tricks

- Utilize CPF Contribution Calculator: Use online tools or calculators to determine the exact amount of ECPF contributions required.

- Timely CPF Submission: Ensure timely submission of CPF contributions to avoid late payment penalties.

- Maximize Voluntary Contributions: Encourage employees to make voluntary CPF contributions to further enhance their retirement savings.

Comparison of ECPF Rates in Singapore and Other Countries

| Country | ECPF Rate |

|---|---|

| Singapore | 17% + 9% + 7% |

| Malaysia | 11% + 7% |

| Hong Kong | 5% + 5% |

| Japan | 10.6% + 5.1% |

| United States | 6.2% + 1.45% |

Future Trends in ECPF Contributions

The CPF scheme is constantly evolving to meet the changing needs of individuals and the economy. Potential future trends include:

- Increased Contribution Rates: Growing healthcare and retirement costs may necessitate higher ECPF rates to provide adequate financial security for employees.

- Age-Based Contributions: CPF contribution rates could be adjusted based on employees’ ages, with higher rates for younger individuals and lower rates for older workers.

- Innovative Retirement Products: Government and financial institutions may introduce new retirement products and incentives to supplement ECPF contributions.

Conclusion

ECPF contributions play a crucial role in ensuring the financial well-being of employees in Singapore. Employers can optimize their ECPF strategies to enhance employee retention, reduce tax liability, and support their employees’ long-term financial goals. By understanding the current ECPF rates, contribution limits, and future trends, employers can make informed decisions that will benefit both their workforce and their organization.

Table 1: ECPF Rates by Account Type

| Account Type | ECPF Rate |

|---|---|

| Ordinary Account (OA) | 17% |

| Special Account (SA) | 9% |

| Medisave Account (MA) | 7% |

Table 2: ECPF Contribution Limits

| Year | Monthly Wage Ceiling |

|---|---|

| 2023 | S$6,000 |

| 2024 | S$6,300 |

| 2025 | S$6,600 |

Table 3: ECPF Contribution Implications for Employers

| Benefit | Impact |

|---|---|

| Employee Retention | Enhanced employee loyalty and retention |

| Tax Savings | Reduction in corporate income tax liability |

| Employee Well-being | Improved financial stability and well-being of employees |

Table 4: ECPF Contribution Implications for Employees

| Benefit | Impact |

|---|---|

| Retirement Savings | Accumulated funds for retirement expenses |

| Healthcare Expenses | Coverage of medical and healthcare costs |

| Housing Needs | Funds for housing down payment or mortgage payments |