Introduction

Deciding between term and whole life insurance can be a daunting task. To make an informed decision, it’s crucial to delve into the nuances of each type and explore which one aligns best with your financial goals and risk tolerance.

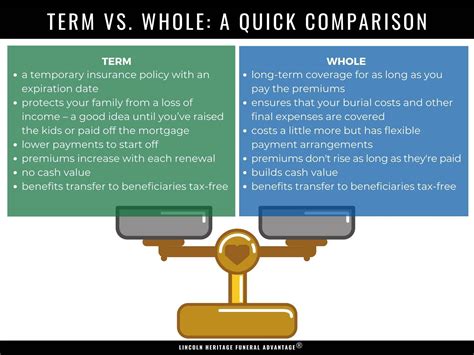

Term Life Insurance: Affordable Protection for a Specific Period

- Definition: Term life insurance provides coverage for a predetermined period, typically ranging from 10 to 30 years.

- Premiums: Term insurance premiums are generally lower than whole life insurance premiums at younger ages.

- Coverage: The death benefit only pays out if the insured person dies within the term period.

- Investment Component: Term insurance does not accumulate cash value.

Pros of Term Life Insurance:

- Affordable: Lower premiums, making it a budget-friendly option.

- Flexible: Customizable term lengths to suit different needs.

- Adequate Coverage: Provides sufficient coverage for the period it’s active.

Cons of Term Life Insurance:

- Limited Coverage: Coverage expires after the term period, leaving no financial protection beyond that point.

- No Cash Value Growth: No opportunity to accumulate wealth through cash value buildup.

Whole Life Insurance: Lifetime Coverage with Savings Potential

- Definition: Whole life insurance provides lifetime coverage, regardless of when the insured person dies.

- Premiums: Whole life insurance premiums are typically higher than term insurance premiums at younger ages.

- Coverage: The death benefit pays out whenever the insured person dies.

- Investment Component: Whole life insurance policies accumulate cash value over time, which can be used for various purposes.

Pros of Whole Life Insurance:

- Lifetime Coverage: Provides financial protection for the entire lifetime.

- Cash Value Growth: Accumulation of cash value offers investment potential and financial flexibility.

- Tax-Deferred Growth: Cash value growth accumulates tax-deferred, creating a tax-advantaged savings tool.

Cons of Whole Life Insurance:

- Higher Premiums: More expensive than term insurance, especially at younger ages.

- Lower Death Benefit: The cash value buildup reduces the death benefit compared to term insurance with the same premium.

- Limited Investment Returns: Cash value growth rates may vary and may not always meet expectations.

Which Type of Insurance is Right for You?

The best choice between term and whole life insurance depends on your individual circumstances and financial goals.

Consider Term Life Insurance if:

- You need affordable coverage for a specific period (e.g., to protect young children or cover a mortgage).

- You have a limited budget and prefer lower premiums.

- You do not require a cash value savings component.

Consider Whole Life Insurance if:

- You desire lifetime coverage, regardless of when you pass away.

- You prioritize cash value growth for financial planning and retirement planning.

- You are willing to pay higher premiums for long-term savings and investment potential.

Comparison Tables:

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Coverage | Time-limited | Lifetime |

| Premiums | Lower at younger ages | Higher at younger ages |

| Death Benefit | Paid only if death occurs within the term | Paid whenever death occurs |

| Cash Value | None | Accumulates over time |

| Investment Potential | No | Yes (tax-deferred growth) |

| Age | Term Life Insurance Premium | Whole Life Insurance Premium |

|---|---|---|

| 25 | $500 per year | $1,000 per year |

| 40 | $1,000 per year | $2,000 per year |

| 65 | $2,000 per year | $4,000 per year |

| Policy Term (Years) | Average Death Benefit |

|---|---|

| 10 | $500,000 |

| 20 | $1,000,000 |

| 30 | $1,500,000 |

| 40 | $2,000,000 |

| Cash Value Accumulation (After 20 Years) |

|---|

| $250,000 |

| $500,000 |

| $750,000 |

| $1,000,000 |

Beyond the Basics

- Hybrid Policies: Some insurance companies offer hybrid policies that combine elements of term and whole life insurance, providing both coverage and cash value accumulation.

- Policy Riders: Additional riders can be attached to term life insurance policies to enhance coverage, such as accidental death or disability income riders.

- Financial Planning: Consider consulting with a financial advisor to determine the best type of insurance for your specific needs and financial goals.

Conclusion

Whether you choose term or whole life insurance, it’s essential to understand the differences and choose the option that aligns with your unique financial situation and risk tolerance. By exploring these choices thoroughly, you can make an informed decision that provides you with the financial protection and peace of mind you desire.