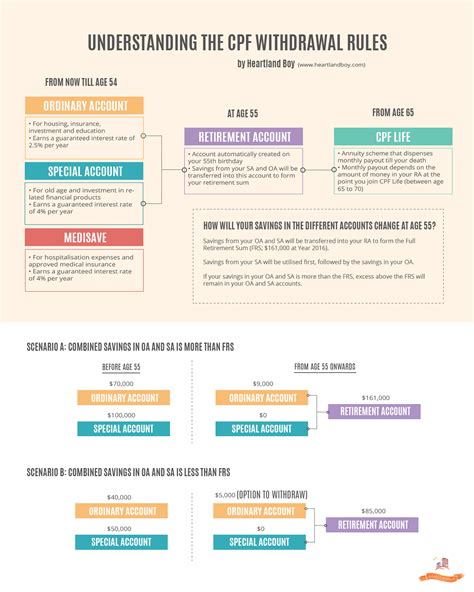

The Basics of CPF Withdrawals at 55

At the age of 55, you become eligible to withdraw money from your Central Provident Fund (CPF) savings. The amount you can withdraw depends on several factors, including your age, employment status, and the balance in your CPF accounts.

Minimum Sum Withdrawal

The first step in withdrawing your CPF savings is to meet the Minimum Sum Withdrawal (MSW). The MSW is the minimum amount of money you must leave in your CPF account until you reach the age of 65. The MSW is currently set at:

- S$196,000 for those born in 1960 and earlier

- S$181,000 for those born in 1961 to 1967

- S$166,000 for those born in 1968 to 1972

- S$151,000 for those born in 1973 to 1977

- S$136,000 for those born in 1978 to 1982

- S$121,000 for those born in 1983 to 1987

Withdrawal Amounts

Once you have met the MSW, you can withdraw the remaining balance in your CPF accounts. The maximum amount you can withdraw is:

- 50% of your Full Retirement Sum (FRS) if you are employed

- 100% of your FRS if you are not employed

The FRS is the amount of money you need to maintain a basic standard of living during retirement. The FRS is currently set at S$279,000.

Table 1: CPF Withdrawal Amounts at 55

| Age | Employment Status | Maximum Withdrawal Amount |

|---|---|---|

| 55 | Employed | 50% of FRS (S$139,500) |

| 55 | Not Employed | 100% of FRS (S$279,000) |

Special Withdrawal Schemes

There are also several special withdrawal schemes that allow you to withdraw money from your CPF savings before the age of 55. These schemes include:

- Home Ownership Withdrawal Scheme (HOWS): Allows you to withdraw money from your CPF savings to purchase a home.

- CPF Education Scheme (CES): Allows you to withdraw money from your CPF savings to pay for your education or the education of your family members.

- CPF Healthcare Withdrawal Scheme (CHWS): Allows you to withdraw money from your CPF savings to pay for your medical expenses or the medical expenses of your family members.

Considerations Before Withdrawing Your CPF Savings

Before you withdraw any money from your CPF savings, it is important to consider the following:

- Your financial needs: How much money do you need to live comfortably during retirement?

- Your other investments: Do you have other investments that can provide you with income during retirement?

- Tax implications: Withdrawing money from your CPF savings may have tax implications.

Frequently Asked Questions

1. How do I withdraw my CPF savings?

You can withdraw your CPF savings online through the CPF website or by visiting a CPF service centre.

2. What are the tax implications of withdrawing my CPF savings?

Withdrawing money from your CPF savings may be subject to income tax. The tax rate will depend on your income and the amount of money you withdraw.

3. Can I withdraw my CPF savings if I am still working?

Yes, you can withdraw 50% of your FRS if you are still working. However, if your CPF savings are above the FRS, you will need to wait until you reach the age of 65 to withdraw the excess amount.

4. What happens if I do not withdraw my CPF savings by the age of 65?

If you do not withdraw your CPF savings by the age of 65, the money will remain in your CPF account and continue to earn interest. You will be able to withdraw the money at any time after the age of 65.

Conclusion

Withdrawing money from your CPF savings at 55 is a major financial decision. It is important to consider your financial needs, your other investments, and the tax implications before you make a decision. By carefully planning your CPF withdrawals, you can ensure that you have a secure financial future in retirement.