Homeownership is a dream for many Americans, but for low-income families, it can seem like an impossible goal. The rising cost of housing, coupled with stagnant wages, has made it increasingly difficult for these families to afford a home. However, there are a number of programs and resources available to help low-income families buy a home.

Government Programs

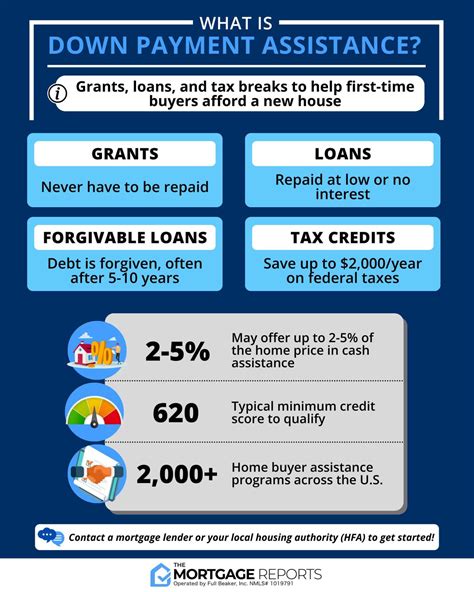

The federal government offers a number of programs to help low-income families buy a home. These programs include:

- FHA loans: FHA loans are backed by the Federal Housing Administration and are available to first-time homebuyers and families with low credit scores. FHA loans typically have lower down payment requirements and interest rates than conventional loans.

- VA loans: VA loans are available to veterans and active-duty military members. VA loans do not require a down payment and have lower interest rates than conventional loans.

- USDA loans: USDA loans are available to families living in rural areas. USDA loans typically have lower down payment requirements and interest rates than conventional loans.

State and local governments also offer a number of programs to help low-income families buy a home. These programs vary from state to state, but they may include down payment assistance grants, low-interest loans, and tax breaks.

Non-Profit Organizations

There are a number of non-profit organizations that help low-income families buy a home. These organizations provide a variety of services, including financial counseling, homebuyer education, and down payment assistance.

Some of the most well-known non-profit organizations that help low-income families buy a home include:

- Habitat for Humanity: Habitat for Humanity is a non-profit organization that builds and repairs homes for low-income families. Habitat for Humanity homes are sold to families at no profit, and families are required to put in sweat equity to help build their homes.

- Neighborhood Housing Services: Neighborhood Housing Services is a non-profit organization that provides financial counseling, homebuyer education, and down payment assistance to low-income families.

- The National Council of La Raza: The National Council of La Raza is a non-profit organization that advocates for the rights of Latino families. The National Council of La Raza offers a number of programs to help Latino families buy a home, including financial counseling, homebuyer education, and down payment assistance.

How to Buy a Home with Low Income

If you are a low-income family, there are a number of steps you can take to buy a home. These steps include:

- Get your finances in order. Before you can start shopping for a home, you need to get your finances in order. This means creating a budget, paying down debt, and saving for a down payment.

- Get pre-approved for a mortgage. Getting pre-approved for a mortgage will help you determine how much you can afford to borrow. This will also give you an advantage when you are shopping for a home.

- Find a real estate agent. A real estate agent can help you find a home that meets your needs and budget. They can also help you negotiate the purchase price and closing costs.

- Make an offer on a home. Once you have found a home that you want to buy, you will need to make an offer. The offer should include the purchase price, the down payment, the closing costs, and the terms of the mortgage.

- Close on the home. Closing on the home is the final step in the homebuying process. At closing, you will sign the mortgage documents and pay the closing costs.

Why Homeownership Matters

Homeownership is more than just a financial investment. It is also a way to build equity, stability, and community. Homeowners have a number of benefits that renters do not, including:

- Tax benefits: Homeowners can deduct mortgage interest and property taxes on their federal income taxes.

- Equity: Homeowners build equity in their homes as they pay down their mortgages. This equity can be used to borrow money, invest for retirement, or pay for college.

- Stability: Homeowners are more likely to stay in their homes for longer periods of time than renters. This stability can benefit children, who are more likely to succeed in school and have positive outcomes in life.

- Community: Homeowners are more likely to be involved in their communities. They are more likely to vote, volunteer, and participate in community events.

Conclusion

Homeownership is a dream that is within reach for low-income families. By taking advantage of the programs and resources that are available, low-income families can achieve the dream of homeownership.

The U.S. Department of Housing and Urban Development (HUD) has announced that it will provide down payment assistance to 10,000 low-income families in 2025. The assistance will be provided through the FHA’s Section 203(b) program, which offers low-interest loans to first-time homebuyers and families with low credit scores.

HUD Secretary Ben Carson said that the down payment assistance will help low-income families overcome the financial barriers to homeownership. “Homeownership is a powerful tool for building wealth and stability, and it is essential that we make it more accessible to all Americans,” Carson said.

The down payment assistance will be available to families who meet the following criteria:

- Annual income below 80% of the area median income

- Credit score of at least 580

- No history of bankruptcy or foreclosure

Families who receive the down payment assistance will be required to take a homebuyer education course and contribute at least 1% of the purchase price towards the down payment.

The down payment assistance will be provided in the form of a grant, which does not have to be repaid. The grant can be used to cover up to 3.5% of the purchase price.

The homeownership rate for Black families has reached a record low, according to a new report from the National Association of Real Estate Brokers (NAREB). The report found that the homeownership rate for Black families fell to 40.6% in 2022, down from 41.6% in 2021.

NAREB President Lydia Pope said that the decline in the homeownership rate for Black families is due to a number of factors, including rising housing costs, stagnant wages, and discrimination. “The dream of homeownership is slipping away for Black families,” Pope said.

The report found that the homeownership gap between Black and white families is widening. In 2022, the homeownership rate for white families was 72.1%, compared to 40.6% for Black families. This gap has been growing wider in recent years.

NAREB is calling on the government to take action to address the racial homeownership gap. The association is recommending a number of policies, including:

- Increasing funding for down payment assistance programs

- Expanding access to affordable mortgage products

- Enforcing fair housing laws

There are a number of down payment assistance programs available to low-income families. These programs can help families overcome the financial barriers to homeownership.

Some of the most common down payment assistance programs include:

- FHA loans: FHA loans are backed by the Federal Housing Administration and are available to first-time homebuyers and families with low credit scores. FHA loans typically have lower down payment requirements than conventional loans.

- VA loans: VA loans are available to veterans and active-duty military members. VA loans do not require a down payment and have lower interest rates than conventional loans.

- USDA loans: USDA loans are available to families living in rural areas. USDA loans typically have lower down payment requirements and interest rates than conventional loans.

- State and local government programs: State and local governments offer a number of down payment assistance programs. These programs vary from state to state, but they may include down payment assistance grants, low-interest loans, and tax breaks.

- Non-profit organizations: A number of non-profit organizations offer down payment assistance programs to low-income families. These programs may include grants, low-interest loans, and homebuyer education.

Saving for a down payment on a home can be a challenge, but it is possible with planning and dedication. Here are a few tips to help you save for a down payment:

- Set a savings goal. The first step is to set a savings goal. How much do you need to save for a down payment? Once you know how much you need to save, you can create a budget to help you reach your goal.

- Create a budget. Creating a budget is essential for saving money. A budget will help you track your income and expenses so that you can make sure that you are saving enough money each month.

- Cut expenses. Once you have created a budget, you can start to cut expenses. Take a close look at your spending and see where you can cut back. Even small changes can add up over time.

- Increase your income. If you can, try to increase your income. This could mean asking for a raise, getting a second job, or starting a side hustle.

- Get help from a financial counselor. If you are struggling to save for a down payment, you may want to get help from a financial counselor. A financial counselor can help you create a budget, track your spending, and find ways to save more money.